While 2Q17 growth was an improvement from 1Q17, much of that reflects the fact that 1Q17 growth was again quite soft, as has been the case in the first quarter in each of the last few years. Take the last two quarters together, and the economy grew at a 1.9% annualized rate in the first half. This is actually an improvement from what we had seen through most of 2015 and 2016, reflecting better performance in the US manufacturing sector over the last three quarters.

Most of the factory-related data we have seen over the last four months show renewed sluggishness in US manufacturing. So, our guess is that the factory rebound that began in summer 2016 is fizzling, and that GDP growth in the second half will come in markedly lower than what we have seen in the last few quarters, say more like 1.5% than the 2.0% pace since 2Q16.

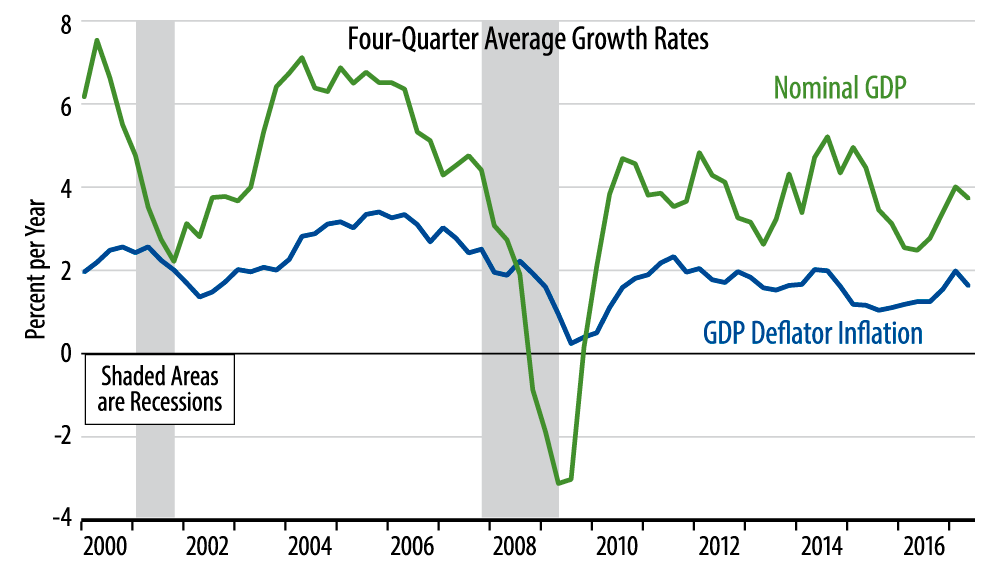

The accompanying chart summarizes our take on inflation. Rather than fixating on labor markets and wage growth, we see US inflation as driven by Fed policy and its effects on total spending in the economy, as reflected by growth in nominal GDP. As you can see in the chart, despite the Fed’s best efforts to revive both real growth and inflation, total spending in the US economy has remained in a 3%–4% growth range throughout the current expansion.

This range of growth is far below what we have seen in any stretch of postwar history. In line with very slow growth in total spending, inflation has remained muted, noticeably less than 2% throughout this expansion.

With nominal GDP growth continuing at a 3.6% rate over the past year, there simply is not enough spending growth to sustain both decent real growth and any acceleration in inflation. Consequently, we doubt that the Fed’s target of 2% or higher inflation will be achieved, regardless of what happens on the unemployment front.