2015年10月29日時点

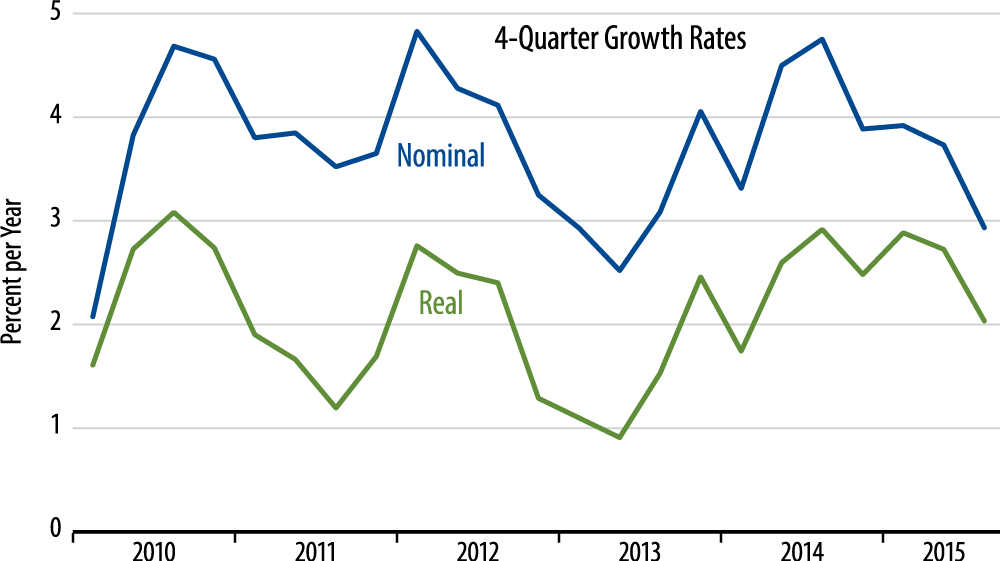

The U.S. Bureau of Economic Analysis today put its preliminary estimate of 3Q15 real GDP growth at 1.5%. Nominal GDP grew at an annualized rate of 2.7%, so that inflation as per the GDP deflator proceeded at a rate of 1.2%. For the last 4 quarters as a whole, the growth rates are 2.0% real, 2.9% nominal and 0.9% inflation.

Many financial market commentators are looking beyond the soggy headline GDP data, pointing out that abstracting from foreign trade and inventory drags, real domestic demand grew at a more impressive 2.9% rate. We are inclined to focus more on the headline number. That slower growth reflects the impact of a phenomenon we have previously highlighted in By the Numbers: the fading US manufacturing sector.

Business and foreign demand for US manufactured goods has softened this year and indeed has been soft for most of the last 4 years, interrupted only by a pickup last year. Domestic consumer demand for goods has grown nicely in 2015, but much of that demand goes to imports, thus providing little boost to GDP. So, the soggier movements in US foreign trade and inventories that putatively held down 3Q15 growth are nothing more than a reflection of factory sector realities.

Those trends were disrupted earlier this year by the incidence of the winter blizzard and port strikes in San Pedro/Long Beach, but they have reappeared in 3Q15 and will likely continue to reassert themselves going forward. The bottom line is that with the manufacturing sector declining, it will be tough if not impossible to sustain decent growth within the goods sectors of GDP.

Meanwhile, the early-2015 spurt in nonresidential construction looks to have topped out, and the housing upturn may soon as well, judging by this week’s new-home sales data. Rising construction activity has offset the drag from manufacturing so far this year, but that may not be the case going forward. We could be looking at one-handle GDP growth on an ongoing basis.