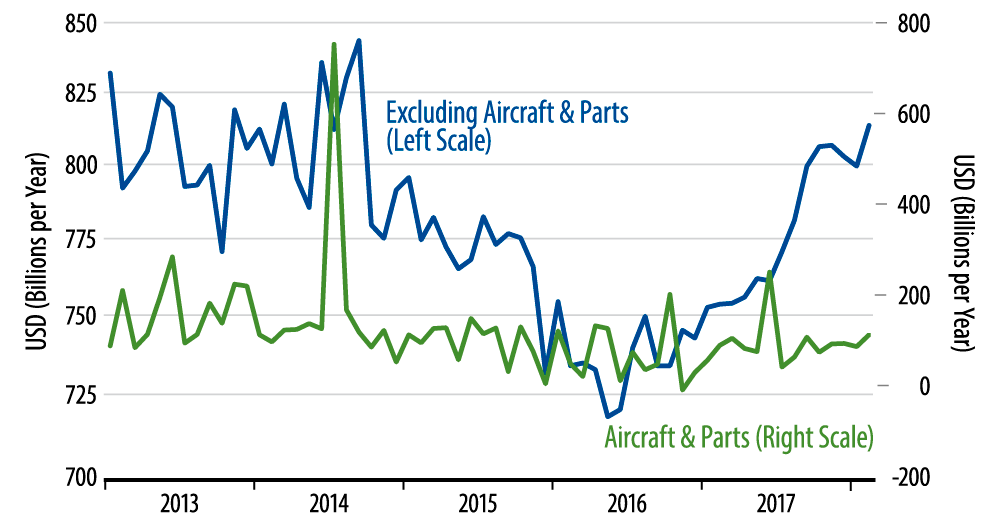

After a four-year stall through mid-2016, both manufacturing and capital spending (CAPEX) resumed growth from mid-2016 through late-2017, only to appear to sputter in recent months. Today’s data suggest that sputter was a temporary blip within an uptrend. As you can see in the accompanying chart, the February gains in CAPEX orders brought this series almost back to its trend since late-2016. Shipments of capital goods are fully back on trend with today’s gains.

In its FOMC press release this week, the Federal Reserve (Fed) mentioned the “moderation” in CAPEX, as well as that in consumer spending. The Fed then largely glossed over these to state that the economic outlook had strengthened in recent months.

We do believe the recent CAPEX sputter was just a temporary pause. However, as indicated in our March 14 By the Numbers installment, we believe the recent softness in retail sales is a return to trend after a brief Christmas binge. We perceive the manufacturing sector as growing modestly and steadily, but that is merely a continuation of the trends of the last 20 months, not a recent improvement.

Meanwhile, construction and services, the other two major sectors of the economy, have both shown slower growth in recent months. So, while we do believe CAPEX in particular and manufacturing in general will grow in the months to come, we disagree with the Fed that economic growth has improved any in recent months.