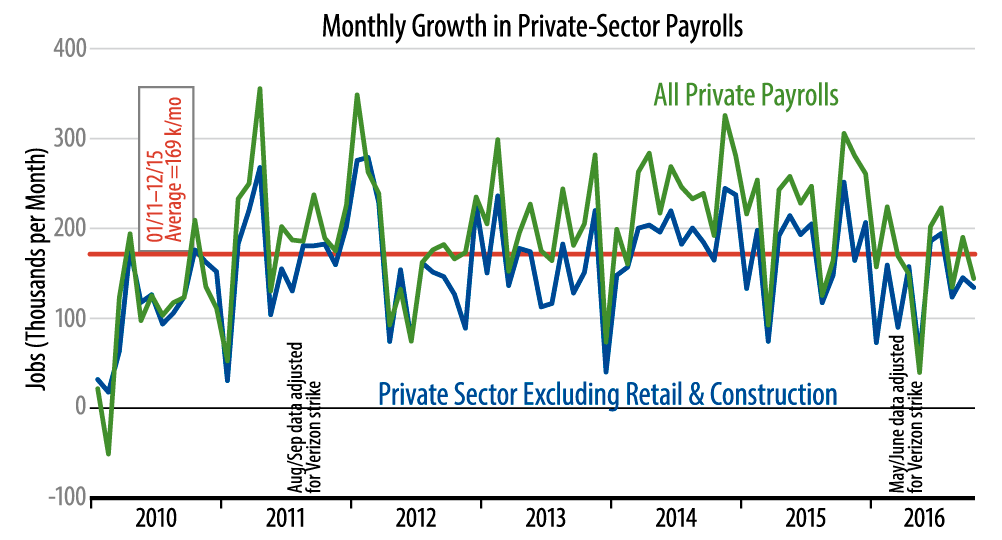

We track more closely a private-sector measure that abstracts from the volatile construction and retailing sectors. That series showed growth of 132,000 jobs in October, alongside 14,000 of upward revisions to September data. For 2016 to date, this measure is averaging 130,000 jobs per month growth, compared with 169,000 per month over the preceding four years.

In other words, job growth continues at a 2016 pace that is markedly slower than the already sluggish pace of recent years. Most market analysts and government officials, however, continue to describe labor market performance as “robust.”

This reminds me of the proverbial frog in a pot of water. If the water is brought to a boil only slowly, the frog won’t know it’s in trouble until it’s too late. In the same manner, while we have seen a marked slowing in job growth this year, there have been no really horrid months, and so many analysts apparently haven’t even noticed the slowing. Yet, it is obvious in any graph of the job data…if one bothers to look.

Another problem with the “all good” attitude toward the job data is the composition of the slowdown. If job growth had decelerated mildly across all industries, the prevailing take might make more sense. The fact is, however, that the slower job growth this year is fully contained within the goods-producing sectors: mining, manufacturing and logistics. There, job growth has gone from mediocre in previous years to distinctly weak in 2016, with manufacturing and mining shedding jobs and logistics seeing only slight growth. And, yes, this goods-sector weakness continued in the October payroll data.

So, yes, October job growth and the Street’s reaction to it are probably positive enough to allow the Fed to hike rates in December. However, the job picture remains soggier than the popular narrative suggests.