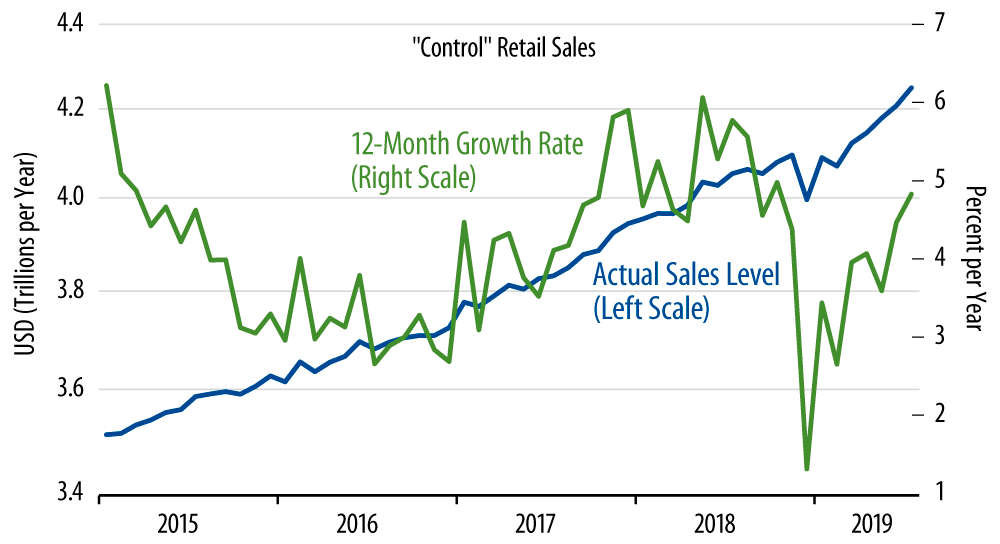

Needless to say, these were strong gains, well above expectations, and they continue a skein of positive retail sales reports over the last three months. With these gains, various store groups are now showing decent growth trends where, just a few months earlier, it looked like their sales were stagnating.

We are referring to grocery stores, restaurants, apparel stores, possibly even furniture stores. All of these groups are now showing decent trend sales growth, whereas three months ago, they looked to be on downward arcs. Meanwhile, yes, online retailers are doing great, with nonstore retailers in toto showing a 16.0% sales gain over the last year. However, they have been doing well all along.

The real turnaround in the last three months has been in the brick-and-mortar, basic-consumption sectors mentioned above. Similarly, while just two months ago it looked like services consumption was flagging, last month’s data put the services sectors in a much better light.

We have been in a strange middle-of-the-road position lately. Early this year, we thought economic growth would underperform expectations and that yields would fall. However, we never bought the recession story that has burgeoned alongside slower growth (and the Fed’s swing from hiking to cutting), and we thought the declining bond yield trend had run its course a month ago, with the 10-year yield just above 2.00%. So, the 45 basis point further decline in bond yields over the last two weeks alongside intensifying recession calls has left us above market expectations on both the economy and yields.

Perhaps today’s strong retail news, along with not-horrible job growth two weeks ago, will provide some counterpoint to recent gloom and put our forecast line less offside relative to market sentiment. No, the consumer alone can’t carry the economy to strong growth. And, yes, much of the strength in retail sales will go to the benefit of foreign producers. Nevertheless, with consumer spending growing decently, there would have to be a lot more weakness in capital spending and housing than we have seen before all the recession talk would start to look correct.