2014年5月06日時点

As with other economic releases, foreign trade data deteriorated during the winter months and have begun to resuscitate with the onset of spring. Trade data are released with an extra month’s lag compared with other indicators, so we only received March data today, just the stirrings of spring, in other words, and not including the yet “warmer” April data for last Friday’s jobs and for other indicators coming in the next few weeks.

Note that unlike other economic indicators, US foreign trade data are dominated by West Coast activity. Each of

the two Los Angeles area ports, San Pedro and Long Beach, individually account for much more activity than any

other US entrepot, and Seattle, San Francisco/Oakland and others are nationally important as well. The point is that

with West Coast ports spared the ravages of the polar vortex, the weather effects on foreign trade flows should be

much less noticeable than those on other indicators such as retail trade, industrial production, or homebuilding.

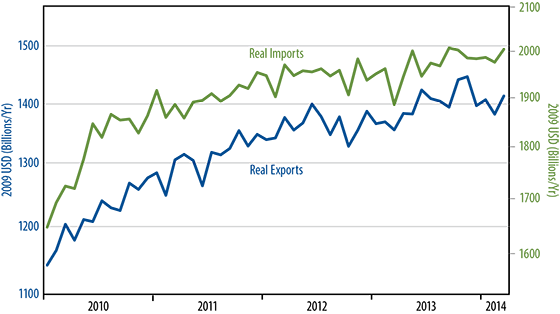

Against all this backdrop, the accompanying chart clearly indicates that export activity flagged over December-February and showed only a fledgling rebound in March. March export levels were still down from November and

essentially unchanged for the last nine months. The March export gains were sufficient to provide some month-to-month improvement in the merchandise trade balance, but not much. Meanwhile, the February trade deficit

was revised lower, but solely due to downward revisions to imports. February exports were actually revised slightly

lower as well.

As with other indicators, not all the winter softness in exports can be attributed to oppressive winter weather, and

while the data generally improved in March, the gains have been less than impressive. To achieve the consensus

3% growth forecast, the US economy has a lot more accelerating to do in the next few months.