2014年6月06日時点

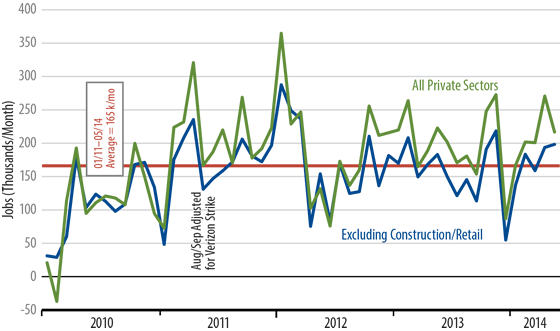

Private-sector nonfarm payrolls added 216,000 jobs in May, and the core jobs measure we track (excluding volatile construction and retail sectors) added 197,000 jobs. The headline tally is down a bit from April, but above the pace of the preceding four months. The May growth in the core measure is the best we have seen in six months.

Then again, for our core jobs measure, the average pace of the last six months (+154,000) is still below the average of the last four years, and this is true of total private-sector jobs as well. (And GDP growth has been less than spectacular over the last four years, averaging 2.2% per year.) In other words, the better job growth of recent months merely serves to offset the especially weak growth over the months from December through February. Similarly, while the unemployment rate continues to edge down, the "employment rate," the percentage of adults who have jobs, remains flat at 58.9%, still below the 59.4% level that held at the outset of the expansion five years ago.

All in all, the recent "recovery" of job growth off winter lows should allay fears that the economy is moving to a yet slower growth path. However, it still does not look as though job growth has recovered enough to be commensurate with ongoing 3% growth in real GDP.

We have been contrarian with respect to growth and bond yields, believing that US growth would not accelerate enough to justify market expectations of imminent (early-2015) Federal Reserve tightening and substantially higher bond yields. We judge that most economic indicators other than payrolls have recently run clearly in accord with our outlook, and conclude that not even the payrolls jobs data, on net, have been at odds with our take.