Retail sales fell 0.1% in December after a more respectable 0.4% gain in November, with that November gain revised up today from 0.2% originally. The control measure we track—excluding cars, gasoline and building materials but including restaurants—was also down 0.1% in December, but November sales for that aggregate were revised downward by 0.1%.

Sales generally declined in Christmas-sensitive areas such as electronics, department and apparel stores. However, the also holiday-sensitive area of restaurants showed a nice gain. Online shopping showed a hefty 1.4% gain in December but this sector is as yet too small to fully offset the softness elsewhere. Books, sporting goods, furniture and building material stores saw decent gains while motor vehicle sales essentially held flat over the last 3 months of the year, following stronger gains early in the year.

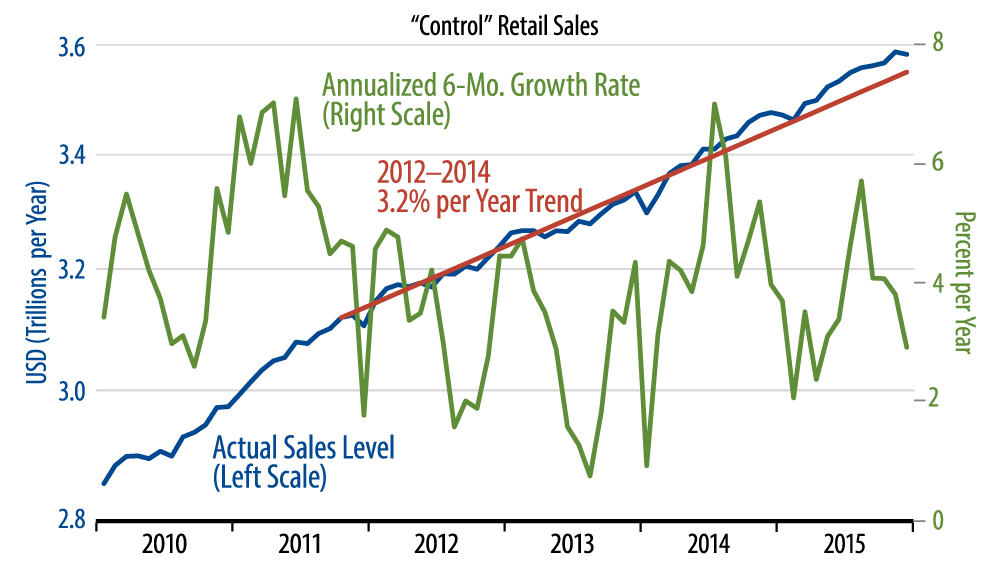

That story of soft 4Q15 sales following stronger performance earlier in the year also applies to the retail sector in general. As seen in the accompanying chart, since August control sales have moved back toward their 2012–14 trend path, after moving well above trend in the middle 4 months of the year.

Still, on net, retail sales finished 2015 with a decent performance. This is in contrast to other sectors of the economy that stumbled in 2015, such as capital spending and exports.

On net, today’s news won’t change the narrative of what is turning out to be a very soft 4Q15 performance. (Our estimate is that 4Q15 growth will be below 1%.) However, even with today’s mini-stumble, retail sales and consumer spending in general are still outperforming the rest of the economy. This, among other things, leads us to be believe that while GDP growth is likely to slow further in 2016, we do not appear to be at risk of a recession.