Most Wall Street pundits and Federal Reserve (Fed) policy officials have convinced themselves that this slower job growth is merely commensurate with the growth rate of the labor force in a full employment economy. As discussed in detail in a recent Western Asset white paper, we take issue with that.

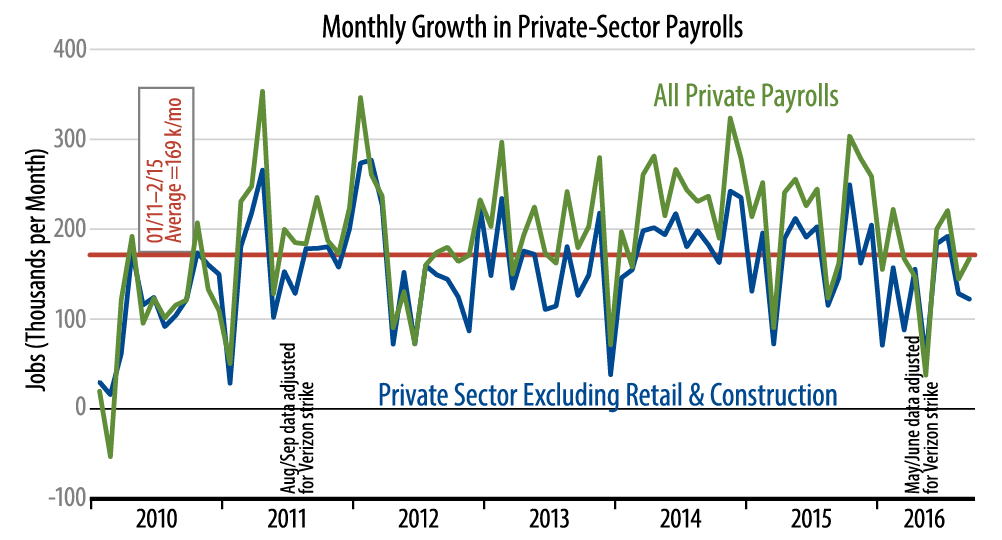

Regardless of who is correct on this score, the fact is that this year’s slowing in job growth has been driven by a contraction in manufacturing jobs and in sectors upstream and downstream from manufacturing: mining, logistics and shipping. So, the slower job growth is symptomatic of problems in US basic industry.

Those problems continued in today’s report, with further September declines and downward revisions to August for these sectors. These swings indicate further declines in industrial production.

As for construction and retailing, it is not that these sectors don’t matter, but rather that their short-term swings are very volatile. These sectors surged at the turn of the year, slumped in mid-year and picked up again in September. On net, they are otherwise steady trend paths.

The economy does not seem to be sliding toward recession at this time, but it is “listing” in the industrial sectors that are critical components of GDP growth. We expect growth to continue in the 1.5% range plus or minus that has been the trend of the last year, and we believe today’s data are consistent with this. And despite Fed rhetoric that present job growth rates are acceptable, we still believe a December Fed rate hike is far from a sure thing.