2014年9月5日時点

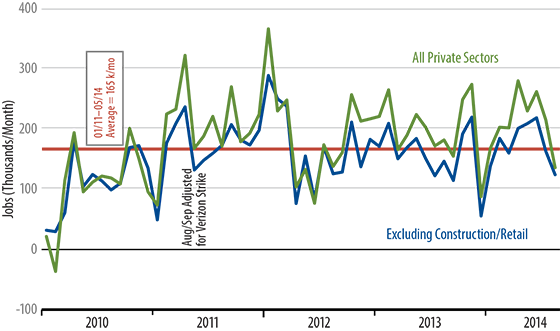

Our take has been that while payroll job growth proceeded at good rates in 2Q14, underlying job growth trends

have been no different from what we have observed for the last four years. Decent trend growth is not the same

thing as accelerating growth, a distinction that seems lost on many analysts.

Yes, growth over April-June was stronger than pre-2014 trends, but that merely-and barely-offset especially

weak job growth in December and January, when the polar vortex was in play. July's data a month ago then pulled

back to 2011-2104 trend rates. August data today stepped a bit below trend.

No, today's data, by themselves, do not amount to a game-changer, but neither did the stronger numbers of 2Q14.

Trends of recent years have been pretty firmly entrenched, and it will make more than a month or two of fluctuations

in either direction before these long-static trends can be said to be broken. So, for now, we continue to contend that

underlying job growth is quite steady, just as are underlying trends for GDP and for most sectors of the economy.

Of course, steady growth is different from the Federal Reserve's (Fed's) expectations of acceleration and sustained,

above-3% growth in real GDP. Our position has been that the data would disappoint the Fed, and nothing in today's

data detracts from that position.

Another question is whether steady 200,000 jobs per month is really that spectacular. We don't see that it is. Yes,

recent growth rates match those of the 2000s, but growth in the 2000s was the weakest in the 100 years covered

by the jobs data. We think the US economy can do much better, and we concur with that element of the analysis

from Yellen and company. The question remains as to when and how that better growth will finally emerge.