The age-old question of whether it’s better to utilize an active or passive investing approach for fixed-income continues to this day. Several years ago, I worked for a corporate plan sponsor. At the start of each year, the plan sponsor’s investment staff would meet to revalidate the strategic asset allocation of the pension plan and, most importantly, discuss the efficacy of various asset classes. As part of that discussion, the staff would validate its confidence in the ability of investment managers for each asset class to produce attractive risk-adjusted returns. The one asset class that perennially had the highest conviction to produce attractive returns was fixed-income and, in particular, broad market fixed-income (US Core, US Core Plus, etc.).

There are several good reasons to support this conviction. For one, in the case of broad market fixed-income, the Bloomberg Barclays U.S. Aggregate Bond Index has 10,398 constituents. And, of course, the largest constituents in the index are the largest borrowers. Doesn’t it seem a bit counterintuitive then that you would hire a passive fixed-income manager that must buy and hold the issuers that are the most indebted? The passive manager cannot express duration, curve, sector or security preferences in the portfolio construction. Considering the index currently has a duration of 5.83 years and a 2.91% yield-to-worst (YTW), it has never been more important to be nimble in the US fixed-income markets (and global fixed-income markets for that matter).

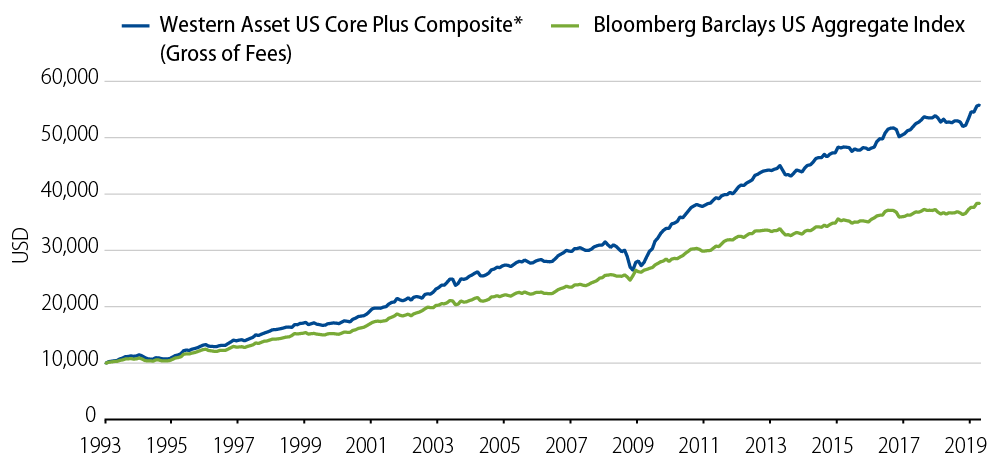

For this reason and many others, the one asset class that simply doesn’t warrant debate of active vs. passive investing is fixed-income. As an example, the chart below represents the performance returns for Western Asset’s US Core Plus investment strategy. Since its inception in 1993, the strategy has generated 150 bps in annualized excess return above its benchmark, gross of fees.

All investors have an investment objective, whether it’s a corporate plan sponsor who needs to meet pension payments or individual employees seeking to enjoy a much deserved retirement. For instance, imagine the growth of your client’s 401(k) plan if their fixed-income assets generated an extra 150 bps per year over a 26-year career for an employee? The math is fairly simple, and it is beyond compelling. If that employee started with $10,000 in 1993, and invested in a broad market strategy that produced an extra 150 bps of return per year for 26 years, she would have $56,000. The passive solution would have generated $38,000 during that same timeframe. I don’t mean to be presumptuous, but I bet that employee would much prefer the $56,000 as this amount could represent a meaningful difference in her quality of life during retirement. Of course, one should expect to pay more for active over passive management, but the appeal is the potential for greater long-term returns.

With asset class return expectations currently being rather modest, it is more important than ever to seek out all incremental sources of return. And that’s where active management in fixed-income comes into play. Yes, it’s fair to say that active managers will not consistently produce 150 bps in excess return every year, but are you really investing your clients’ retirement assets based upon what happens in a single year? We all know that financial advisors and plan sponsors are investing assets for the long term and that’s what counts.

Is the active versus passive debate still alive? Yes, of course it is. But, when it comes to fixed-income, it’s not really a worthwhile debate.

View the Performance and Risk Disclosures for Western Asset’s US Core Plus strategy.