Fixed-income investors face a variety of questions; among them perhaps none is more important than the question of risk and reward. How much am I being compensated for the amount of risk that I am taking? How does that compare to all of the other opportunities out there? Given current market dynamics, short-term credit stands out as one of the more attractive opportunities today.

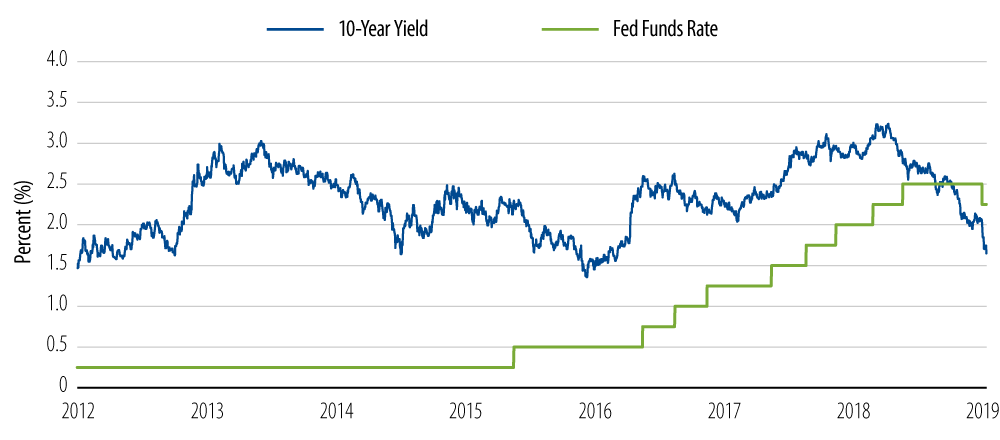

Since late 2015, the Fed has raised front-end interest rates by a total of 225 bps or 2.25%. This has caused short-term corporate bond yields to rise. At the same time, intermediate and longer-term corporate yields have stayed in almost exactly the same place. What this does is provide investors with a decent amount of yield without forcing them to take duration risk or longer-dated credit risk.

Consider these numbers: Historically speaking, investors have been able to pick up an additional 300-400 bps of yield by extending further out the maturity curve, a relatively decent amount of compensation for the risk. However, that number has shrunk to just 140 bps of additional spread compensation for extending as much as 30 years. Not only do investors have the added duration risk of a longer-dated bond (could be as much as 16 years' worth), but there is also the added risk of investing in a corporate bond out to that long maturity date. The longer the maturity, the less transparent the business will be—another factor that makes front-end credit the more compelling place to be.

A question about short-term credit that we get asked often is "why now?" There are a few reasons but none bigger than the unprecedented dovish pivot by the Fed this year. At the end of December, it seemed as if the Fed would continue on its hiking path for the next couple of years. However, here we are just six months later and the Fed has made its first interest rate cut in a decade, a stunning dynamic for market participants to digest. This will create more demand for the front end of the yield curve and ultimately drive these yields lower. We think this opportunity will not be around for long.

Of course, while all of this has been occurring here in the US, the rest of the world has seen interest rates march lower and lower, in many cases into negative territory, such that there is now over $15 trillion dollars' worth of negative-yielding fixed-income assets (or 30% of total fixed-income around the globe), another remarkable development for investors to grapple with. The search for yield is becoming a global crisis.

So for investors who are considering credit but want to avoid duration risk, or for investors who want exposure to credit but are perhaps concerned with recession risk, we believe front-end credit offers a very attractive risk/reward opportunity. There are a variety of ways to gain exposure to this, whether through a mutual fund or an ETF, and a few that will pay over 3.50% with a duration of less than 3 years. Funds such as these typically offer a generous coupon without requiring the investor to take additional duration and credit risk, and can make for an excellent diversifier for most any portfolio.