As we wrote about recently regarding pandemic-driven changes to the office sector, the hospitality sector overall, and hotels specifically, must also adapt to the new environment or risk extinction. In our view, there are many parallels between the future of the office and the future of hotels. Both need to consider foremost the safety of their customers and offer appealing modifications to attract and retain business in a sustainable manner. While everyone is still very much figuring out what makes the best sense in the post-pandemic world—post onset that is, as we cannot speculate on any imminent pandemic “end”—we believe the right approach could help hotels rebound from the crushing blow of COVID-19 and eventually regain their market share.

Here we describe three of the factors that we think will be the most significant in shaping the hospitality sector of the future (and indeed, the present).

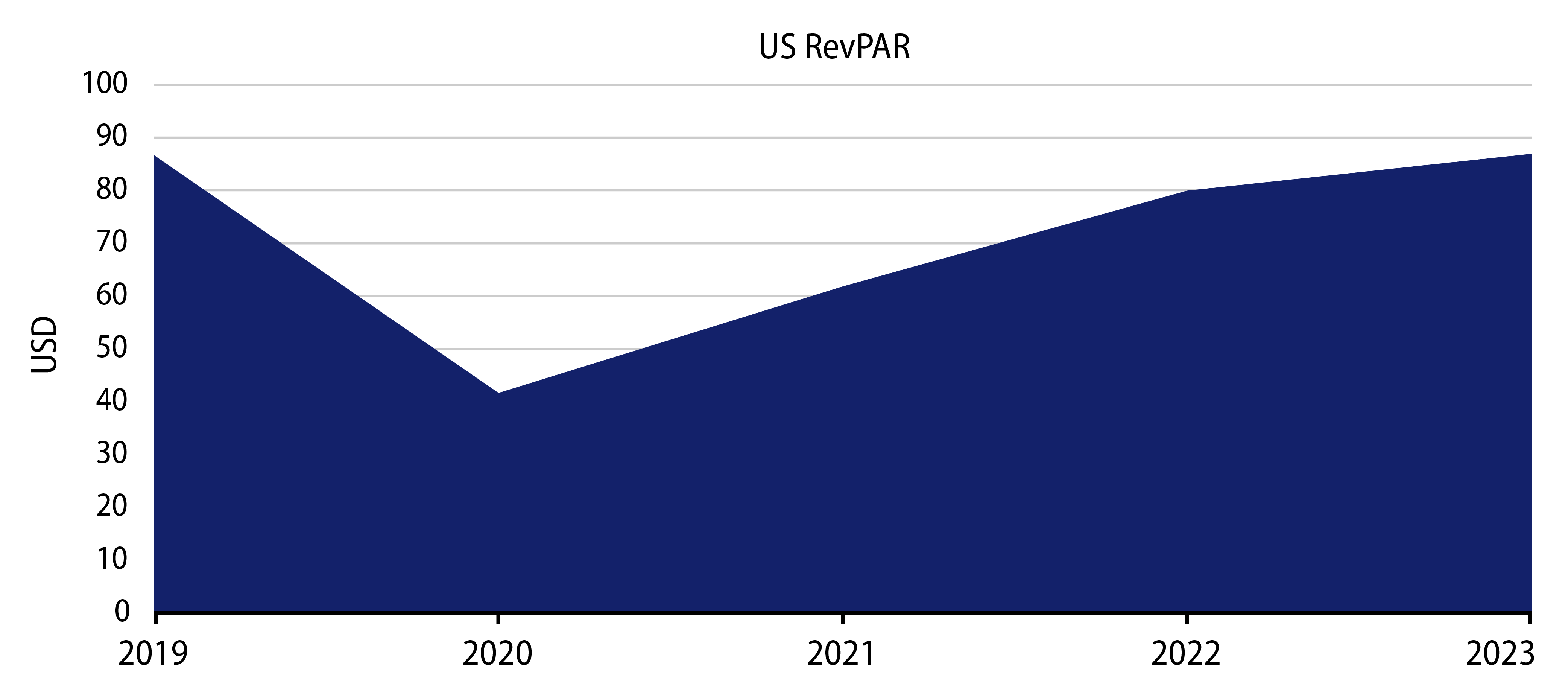

We are encouraged by the partial recovery hotels have made in the last two months as properties have reopened, but the road ahead to a full recovery will be long and likely not very smooth. Revenue per available hotel room across the industry is expected to fall by more than half this year compared to last. Even with what could be a robust recovery next year, we believe it will take three to five years for the national measure to climb back to 2019 levels.

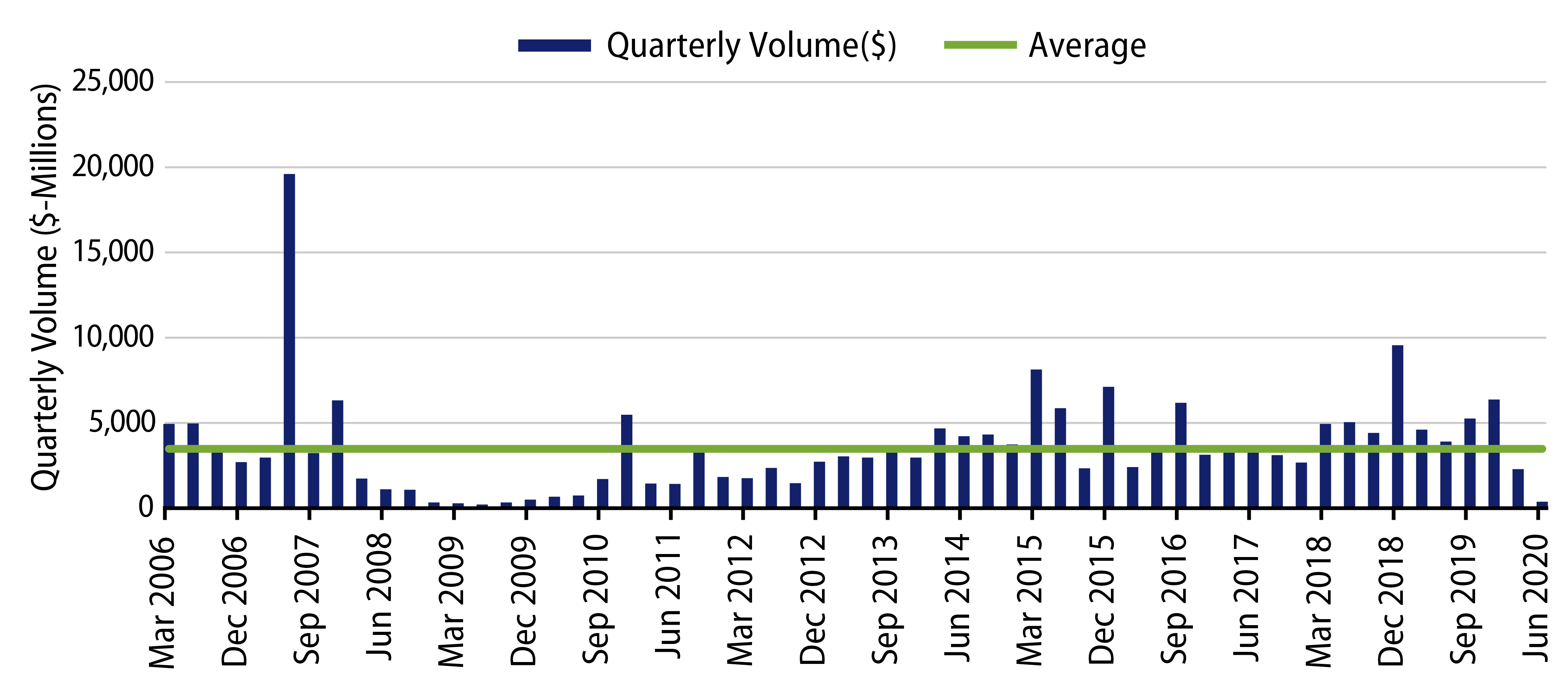

Uncertainty regarding the shorter- and longer-term outlooks have led to a near complete collapse in hotel transactions. Less than $300 million of hotel properties were sold across the US in 2Q20, which was the lowest quarterly total since 3Q09 and well short of the $3.5 billion long-term average. We expect the dearth of transactions will continue for another quarter before beginning to increase, driven by potentially billions of dollars of distressed sales. This lack of transaction volume poses another challenge across the industry and for investors as there will be limited pricing transparency for both assets and the related financing. As a result, we expect the recovery period for hotel performance to be stronger and to occur sooner than the recovery for the financing and investment of the assets. In this regard, the current crisis and its aftermath will be unique.

Exceptional cleanliness to minimize viral spread will continue to be an important focus for customers and operators alike. Improvements in air filtration systems for common areas and rooms are a given. Digital room keys as well as contactless doors, sinks, toilets and elevators will also likely become the norm and in some cases are already in place. We expect some properties will replace rugs in guest rooms with hard surfaces that are easier to sanitize, such as tile or wood floors. Many of these improvements will be expensive and lead to inflated capital expenditure budgets in the near term, but we expect the improvements to help generate attractive returns on the investments. What’s more, operators that do not invest in these upgrades will suffer over time from persistent and significantly lower occupancy levels.

The transformation of these assets over time will likely have a number of positive economic and social benefits, and as the “dust settles” these trends will accelerate. The longer-term outlook for demand and its impact across the industry will depend on how long-lasting recently observed changes in behavior become. For example, corporate and group travel has been essentially non-existent since February and is expected to remain near zero for the balance of the year. Will corporations resume travel next year and do so at the same level they did pre-Covid? That’s unlikely to be the case for a number of years, if ever. Similarly, conferences are an important channel of business that impacts every department within a hotel and that business has ground to a halt; many conferences have canceled 2020 events and even those in 2021. We expect over time this demand driver will return to 2019 levels but that the recovery will take a minimum of two to three years. In the meantime, the related lack of revenue and profit will adversely impact a select group of properties in a handful of markets.

At Western Asset, we have had a relatively cautious view regarding hotels for the last two years and as a result have only invested in a select number of properties during that time. The challenges facing the sector today are unprecedented in their size and scope. However, we believe the combination of changes to the operation of the properties, the future economic recovery, potential for more direct stimulus through government legislation and our team’s approach both pre- and post-investment will lead to favorable risk-adjusted returns for our clients.