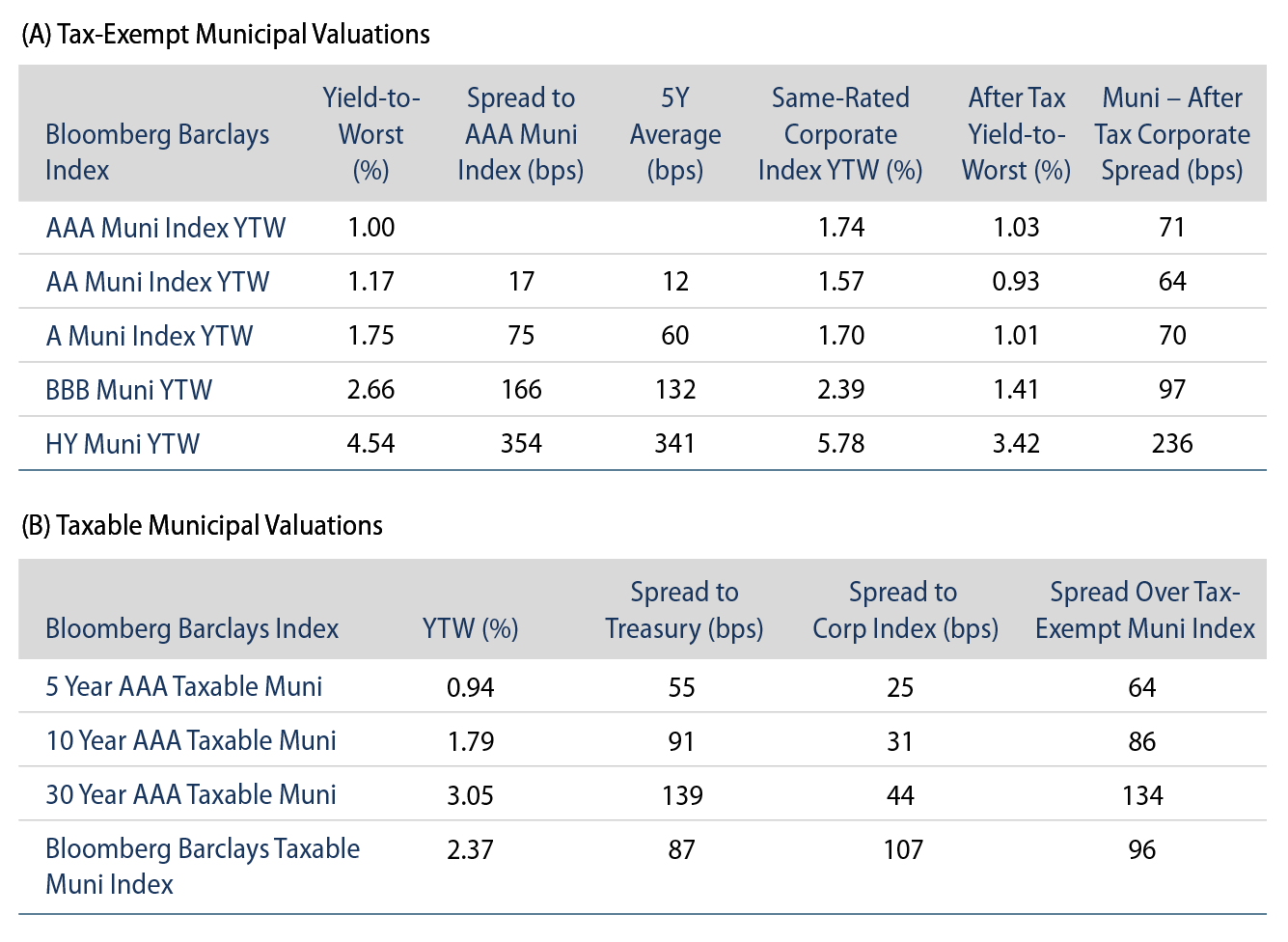

Municipals Posted Positive Returns as the Curve Flattened

The monthly municipal supply just made a new record. AAA municipal yield changes were mixed as the yield curve flattened. The Bloomberg Barclays Municipal Index returned 0.08%, while the HY Muni Index returned 0.15%. This week we feature three key state tax reform initiatives on the ballot.

October Marks a Record Month of Municipal Issuance

Fund Flows: During the week ending October 28, municipal mutual funds recorded a fourth consecutive week of net inflows, with $582 million, according to Lipper. Long-term funds recorded $206 million of outflows, intermediate funds recorded $88 million of inflows, and high-yield funds recorded $100 million of inflows. Municipal mutual fund net inflows YTD total $25.6 billion.

Supply: The muni market recorded $18.1 billion of new-issue volume last week, down 6% from the prior week. October supply set a new record for monthly issuance at $78 billion, approximately 10% above the prior record observed in December 2017. Issuance of $415 billion YTD remains over 30% above last year’s pace, mostly driven by higher taxable issuance. Next week issuance drops significantly to $621 million. Largest deals include $130 million Maine Turnpike Authority and $97 million City of Grand Island Combined Utilities transactions.

This Week in Munis: Election Day

From tax policy to infrastructure initiatives, changes to federal policy can drive broad municipal market implications, as discussed in Western Asset’s 2020 Election Outlook. Elections also bring voter-approved state and local policies which can impact the trajectory of individual credits in the muni market. Here we discuss three key state reform initiatives ahead of the national election.

California

Proposition 15 is a proposed structural reform to amend the existing Proposition 13, a landmark tax rule passed in 1978 that limits property taxes to 1% of assessed value and property tax increases to no more than 2% per year unless the property is sold and reassessed. Prop 15 would revise this system to raise taxes on large commercial entities. Specifically, owners of commercial properties with a combined value of $3 million would be assessed at fair market value at least every three years.

The impact would be significant. According to the independent Legislative Analyst’s Office, passage of Prop 15 would net an estimated $6.5 billion to $11.5 billion per year once full implementation is in place by 2025. The new funding would be split 40% toward public schools and community colleges, and 60% toward local governments. However, not all counties will reap the benefits. Counties with abundant commercial activity, such as Los Angeles, Santa Clara and San Mateo would gain considerably, but rural counties such as Sierra, Trinity and Calaveras would not reap similar benefits.

The initiative has gained traction with recent endorsements from Joe Biden and California Governor Gavin Newsom, which could spark a voter base that has demonstrated a willingness to pass tax hikes. However, the timing of a major tax reform in the middle of a pandemic may serve as a headwind for this legislation.

Illinois

A gradual income tax initiative on the ballot in Illinois seeks a voter reversal of the constitutionally mandated flax tax in the state. The proposal would lower the tax rate from 4.95% to 4.90% on those earning between $10,000 and $100,000, hold the rate at 4.95% for those earning between $100,000 and $250,000, and increase the rate to 7.75%-7.99% for filers earning above $250,000.

Under this proposal, only 3% of Illinois residents would pay higher income taxes, enhancing its attractiveness to the majority of voters. However, there has been well-funded opposition, arguing that the reversal of this amendment would open a Pandora’s Box of future tax increases.

The graduated tax increase proposal is likely the most significant ballot initiative for the municipal market, given the revenue needs of the state of Illinois to address structural budgetary issues, exacerbated by pandemic conditions. Without the passage of the tax, we would expect the state to be downgraded to below-investment-grade territory by at least one major rating agency.

Colorado

Proposition B would remove the Gallagher Amendment, which has kept residential property taxes low in Colorado by limiting residential property tax collections to 45% of the state’s overall tax base, with nonresidential properties comprising the remaining 55%. When home values rise faster than business property values, the state constitution triggers a cut to the residential assessment rate, which determines residential tax collections.

Colorado homeowners have saved an estimated $35 billion in residential property taxes since adoption 1982. Last year alone this represented a $2.8 billion tax cut. Currently, business properties pay about four times more than residential homeowners, and this is anticipated to go up to five times next year.

Strong migration trends within the State of Colorado have contributed to residential home values exceeding commercial real estate, resulting in statewide assessment rate declines. While certain areas of the state have benefited from favorable migration patterns and tax collections, lower statewide residential assessment rates are often a strain on rural areas that have not benefited from the same migration patterns.

Gallagher is expected to trigger an additional $491 million in cuts to school districts and $204 million in cuts to county governments. If Gallagher remains in place, the residential assessment rate is expected to decrease by 18% in 2021, which would rate as the second largest property tax cut in the state’s modern history. Under this scenario, we would remain cautious on local general obligations in rural areas of the state.