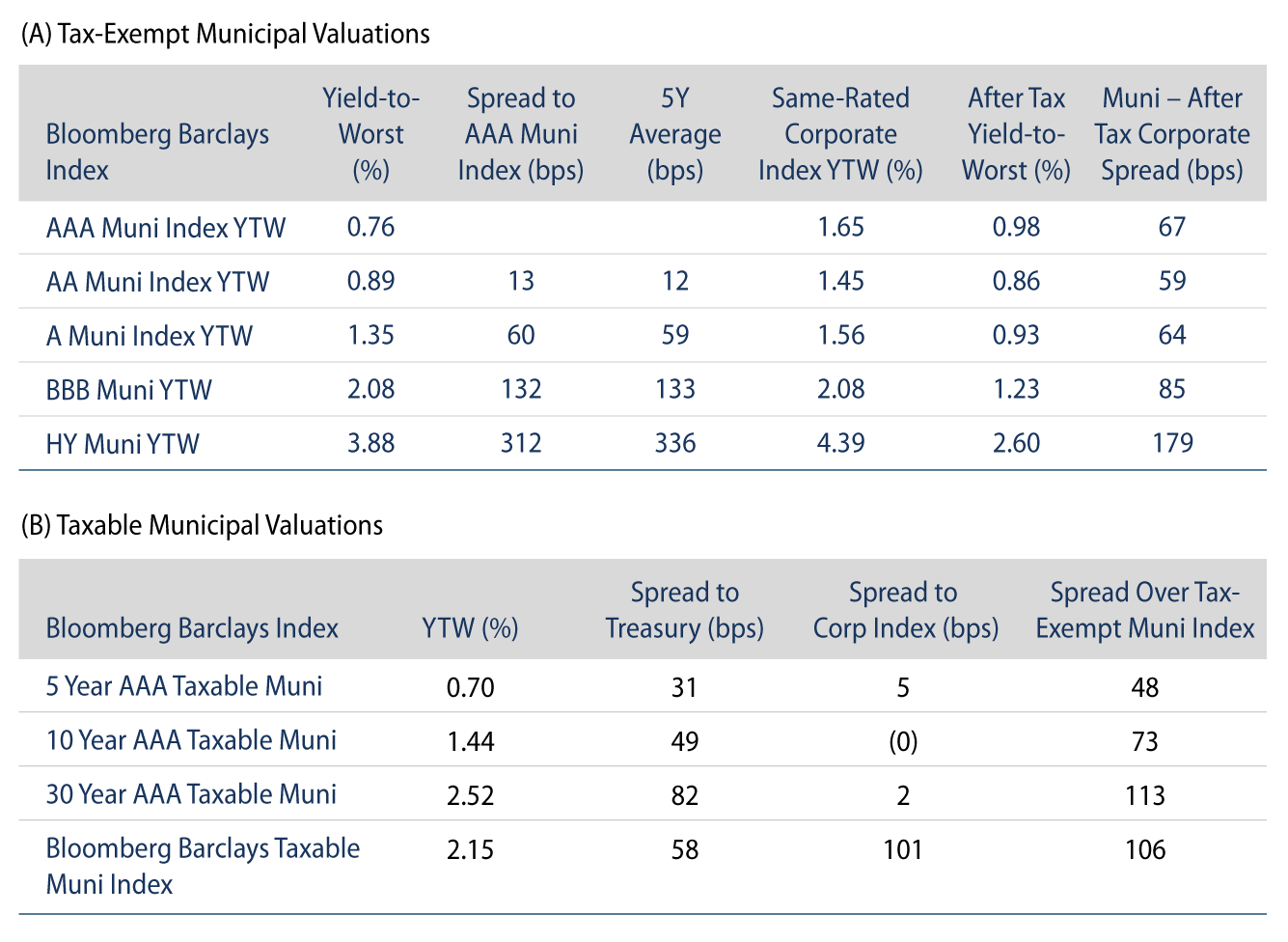

Municipal Yields Were Roughly Unchanged

Municipal yields moved slightly higher in intermediate and long maturities, but outperformed Treasuries. Fund flows remained positive and supply was elevated as issuers took advantage of the year’s last full week of trading. AAA municipal yields moved 1 bp higher in intermediate and long maturities. Municipal/Treasury ratios grinded tighter as Municipals outperformed Treasuries. The Bloomberg Barclays Municipal Index returned 0.12%, while the HY Muni Index returned 0.28%. This week we address recent health care price-gouging issues highlighted by a popular news outlet.

Municipal Technicals Maintain Strength, Supported by Positive Fund Flows

Fund Flows: For the week ending December 16, municipal mutual funds recorded a sixth consecutive week of inflows, reporting $915 million of net inflows, according to Lipper. Long-term funds recorded $675 million of inflows, intermediate funds recorded $33 million of outflows and high-yield funds recorded $277 million of inflows. Municipal mutual fund net inflows YTD total $36.7 billion.

Supply: The muni market recorded $12.5 billion of new-issue volume last week, down 10% from the prior week but above average as issuers took advantage of the last non-holiday week of the year. Issuance of $470 billion YTD is up 16% year-over-year, primarily driven by higher taxable issuance. There is a very limited new-issue calendar this holiday-shortened week, with expected issuance of just $103 million.

This Week in Munis: Health Care Headlines

Last Sunday, a popular news program highlighted controversy around a large health care system violating anti-trust laws through price gouging practices after gaining monopolistic market share in its region. A suit brought by the California state attorney general resulted in a pending settlement of $575 million.

As mentioned in our recent blog, Healing Healthcare, the consolidation of the health care sector has driven scale and improved the credit profile for many large health care systems as changing payment methodologies have driven reimbursements down. Western Asset believes that the growing scale of health care systems is inevitable and that market dominance is in fact a positive credit factor that has driven risk-adjusted value to the sector. However, predatory prices and related practices such as overbilling have led to adverse outcomes, including rating downgrades associated with heightened regulatory and litigation risk.

We believe this case underscores the need for rigorous credit discipline, and that overbilling highlights just another ESG risk variable worth monitoring in the fragmented municipal market. Western Asset’s issuer-level credit analysis incorporates an assessment of management and billing practices to protect investors from these litigation and regulatory risks. Prior litigation, contract disputes with health care insurers and labor disputes can all signal a hospital that is more focused on the bottom line than delivering quality care. As the nation moves toward rewarding providers for quality of care rather than quantity, achieving scale without delivering cost savings to customers will not be a sustainable strategy.