2015年04月29日時点

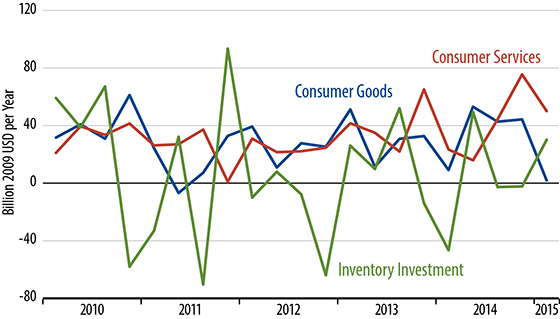

First quarter 2015 real GDP growth was reported +0.2% this morning, below the already-depressed consensus estimates of +0.7% to +1.7% and further below the +2.4% average for 2014. 1Q15 growth was held down by weakness in consumer spending on goods, by a large decline in the trade balance, and by a huge decline in nonresidential construction. At the same time, inventory investment showed a very large increase, and consumer spending on services also rose strongly, thanks to weather-related gains in utilities spending and a surge in health care spending (that also boosted 4Q14 growth).

In other words, the “temporary” factors serving to boost 1Q15 GDP look to be about as large in magnitude as those reducing 1Q15 growth, and still overall growth came in near zero. The expectation from most Wall Street analysts has been that while 1Q15 growth would be soft, there would be a sharp rebound in 2Q15. This is, indeed, what happened last year, when -2.1% 1Q14 growth was followed by +4.6% growth in 2Q14.

However, the chances of a similarly sharp rebound in 2Q15 look remote. Warmer 2Q15 weather will bring a reversal of 1Q15 increases in utilities spending. The 1Q15 health care spike is reportedly due to another surge in Medicaid enrollment (first anniversary of Obamacare) and will likely fizzle in the spring months, just as happened a year ago after the initial launch of Obamacare.

Finally, as argued in our 4/14/15 installment of “By the Numbers,” the 1Q15 softness in retail sales—thus in consumer spending on goods—looks more like “payback” from overstated 4Q14 gains than a weather-related decline. If this is indeed the case, then a sharp 2Q15 rebound in consumer goods spending is unlikely.

No, the US has not downshifted to a zero-growth trend. However, it looks as though there was only a small net drag, at most, from the weather on 1Q15 GDP growth. There is a good chance that growth for all of 2015 will come in decidedly slower than even the meager 2.3% average pace of the last five years.