So where did the robust GDP growth come from? Mostly from some unusual suspects: inventories and foreign trade. Inventory accumulation boosted 1Q19 growth by 0.7%, while net exports provided a 1.2% boost. In other words, net of these "one-offs," 1Q19 GDP growth would have been about 1.3%, close to the expectations bandied about not so long ago.

The consumer spending numbers were a little better than expected. For goods consumption, I had expected a much sharper decline than the -0.7% drop reported, despite the strong March retail sales print last week. Apparently, the components of retail sales were more favorable for consumer spending than we perceived. Remember, with the effects of the government shutdown, we hadn’t gotten any official word on consumer spending past the January data until the news today covered data through March.

Another factor serving to boost real growth was price declines. Prices of consumer goods declined at a -1.7% rate in 1Q19, compared to a +0.2% rate of change over the preceding four quarters. Indeed, the GDP deflator, the inflation rate for everything included in GDP, posted just a +0.6% annualized rate of increase in 1Q19, compared to a +2.2% rate over the prior four quarters.

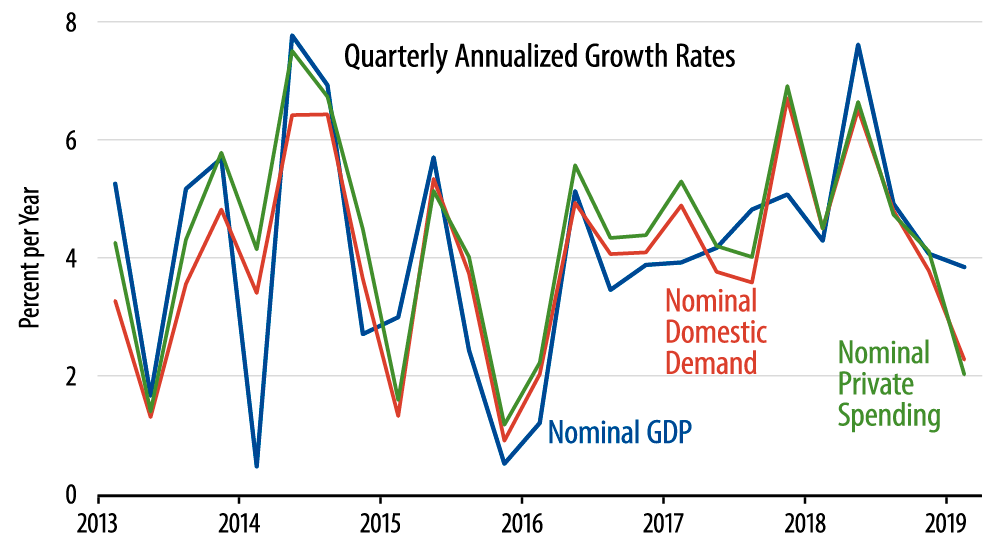

Toting things up, real GDP grew at a 3.2% rate in 1Q19, but nominal GDP at just a 3.8% rate. Excluding inventory investment, real final sales grew at a 1.3% rate, while nominal final sales grew by 2.0%. Excluding both inventories and foreign trade, real domestic demand grew at a 1.2% rate, while nominal domestic demand grew 2.3%.

As seen in the chart, nominal growth rates for the various spending measures have been slowing for quite some time. This indicates first that overall economic growth is indeed slowing AND second that inflation is in no danger of heating up. Forget what is going on with unemployment; when final demand—aka nominal spending—is slowing, faster price increases simply won’t fly.

As for overall GDP growth, any careful look at the details shows that this is not a sugar high. However, neither is the 1Q19 pace sustainable. As the "one time" boosts to growth from inventories and trade fade—and even with better consumer spending growth than that of 1Q19—underlying GDP will settle in the low 2% range. At least, that is my take.