2015年07月30日時点

Today's second quarter 2015 GDP release was widely anticipated, both because it featured benchmark revisions of data back to 2012 and also because analysts were eager to see how much of the first quarter weakness in growth was revised away and/or reversed by second quarter strength. The answer is: not much.

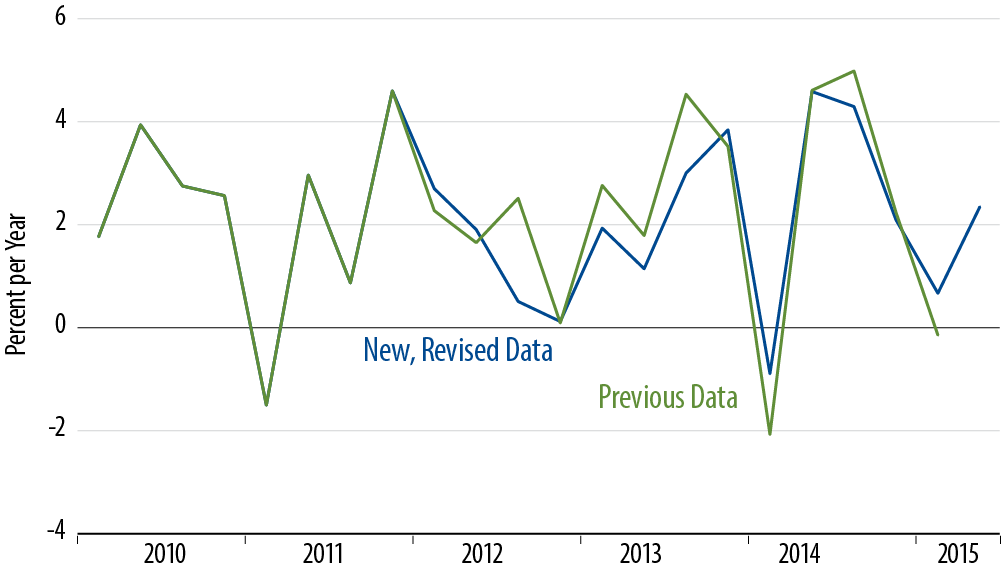

Yes, 1Q15 was revised up from -0.2% to +0.6%, but even the revised rate is a miserable performance. What's more, there was not much reversal in 2Q15, which showed growth of only 2.3%. Combine them, and real GDP growth averaged only 1.5% in the first half of 2015, compared with 2.4% for all of 2014.

What's more, the revisions downgraded growth over 2012-2014 by a total of -0.9 percentage points. As seen in the first chart, real GDP growth was noticeably slower in late-2012 and early-2013 than previously reported. The changes to 2014 are mostly changes in seasonal adjustment, with the 1Q14 decline revised to be less weak and so the 2Q14/3Q14 rebound revised to be less strong, with only a slight +0.1% change to overall 2014 growth.

For one thing, 3Q14 growth was boosted by a very strong increase in vehicle production, brought on by a short model-year changeover. This year, in contrast, we have already seen a sharp increase in vehicle production in the 2Q15 data, and also, the shorter model-year changeover is likely now "baked into" the seasonal factors for vehicle production, thanks to the 2014 experience.

Also, 3Q14 growth was buoyed by "September spending" on national defense, which showed a big increase in 3Q14, only to fall back in 4Q14. We are less likely to see such a swing this year.

Finally, and most importantly, as we have previously remarked in By the Numbers installments, there has been a much more substantive slowing in US factory sector growth this year than was the case a year ago. This manufacturing slowdown is likely to show lingering effects on growth over the rest of this year.

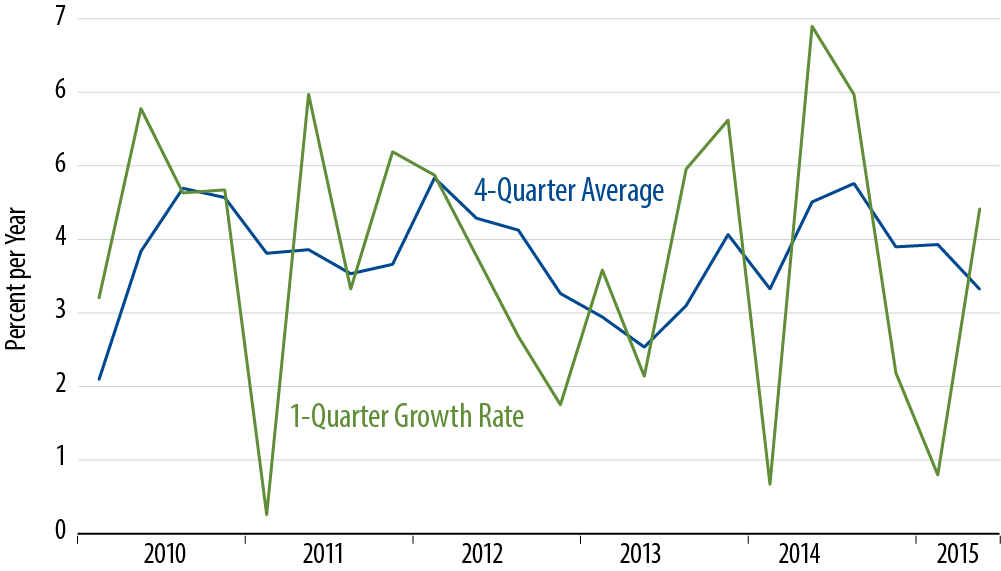

The final chart shows current trends for nominal GDP growth: that is, real growth plus inflation. With real growth slowing and inflation slowing as well, nominal GDP growth has decelerated pretty dramatically over the last year. Many folks, ourselves included, would see this slowing as a meaningful driver of bond yield levels.