As you can see, the quarterly pattern of growth now looks a lot different. From a bit longer-term perspective, average growth for the four quarters of 2017 was revised from 2.5% to 2.8%, while that for the four quarters of 2018 was revised from 3.0% to 2.5%. 1Q2019 growth was not revised, not surprising given that BEA has no more "background" data on 1Q now than it did before.

After getting a chance to review the details of 1Q2019 growth a few months ago, we came to the conclusion that 1Q growth was vastly overstated. The GDP data indicate extremely fast—9.1%—1Q growth in the goods sectors: manufacturing (excluding vehicles) and mining. Yet, Fed data for these sectors indicate negative output growth in 1Q. With this kind of discrepancy, it was hard to see the 1Q GDP data as credible.

We thought we would get some reversal of this anomaly in 2Q, but it didn’t happen. Today’s data indicate a 2.7% growth in goods sector GDP in 2Q, even while Fed data show further, slight declines in goods-sector output then. So, no reversal of the apparent overstatement of 1Q. We have to acknowledge the Street conclusions that reported GDP growth has exceeded expectations across the first half of the year, but we would at the least put an asterisk after that admission.

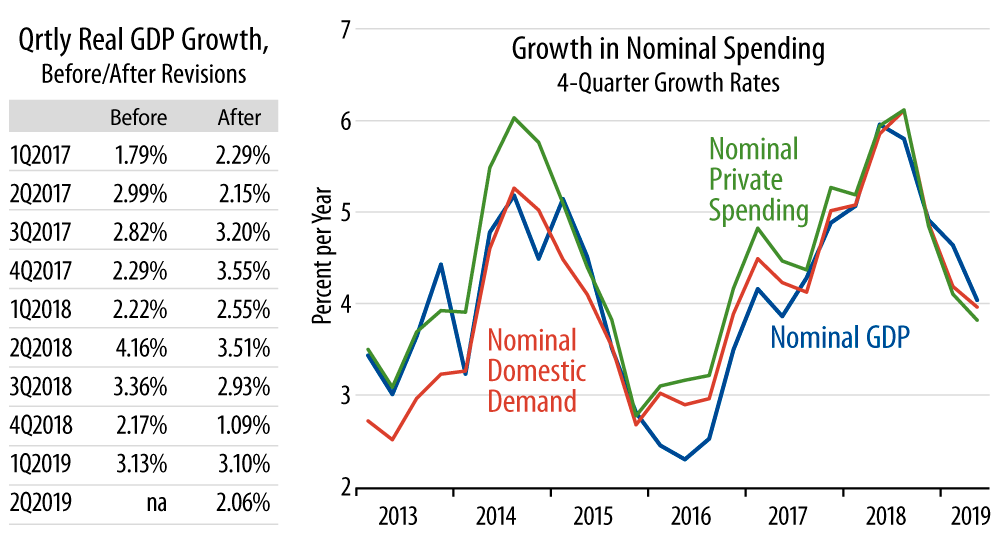

Meanwhile, the 2Q data continue a trend we discussed when the 1Q data were released in April. Despite the relatively favorable news on real growth, nominal GDP and all nominal spending measures continue to decelerate. As seen in the accompanying chart, all these measures show about 4% growth in nominal spending over the last year.

Forget about whether unemployment is below your perceptions of normal or whether real growth exceeds your expectations of sustainable. If nominal spending growth is not rapid nor accelerating, there simply is no room in the economy for inflation to accelerate (unless growth were to collapse, which would then put downward pressure on prices). The nominal spending data are proof positive that Fed efforts to accelerate growth and inflation are failing. In other words, today’s data continue to point to continued below-target inflation.