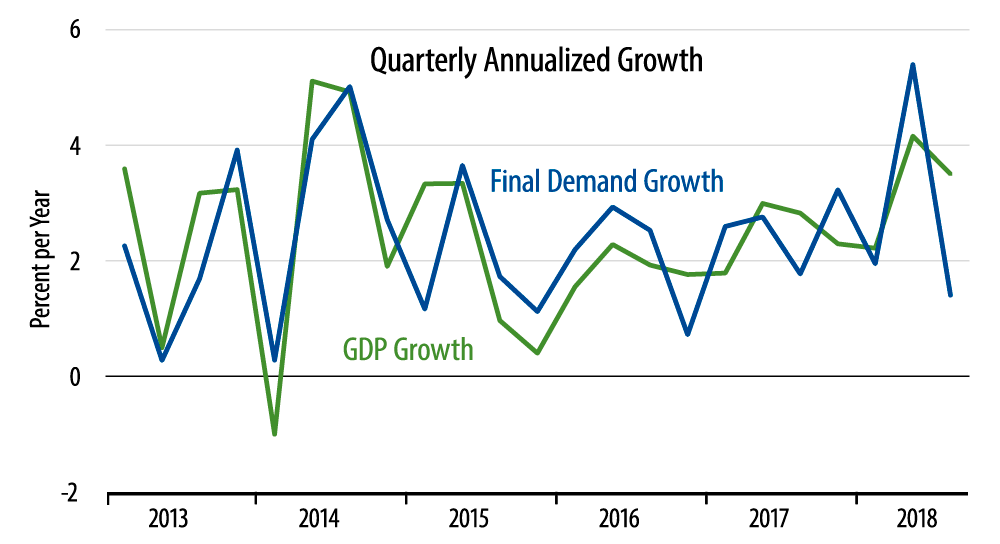

The 3.5% 3Q18 GDP growth was down slightly from the 4.2% pace of 2Q18. The real final demand growth of 1.4% was down sharply from a rate of 5.4% in 2Q18.

On the negative side, the foreign trade balance swung sharply downward in 3Q18. Foreign trade had provided a +1.2% boost to GDP growth in 2Q18, but it contributed a -1.8% drag on growth in 3Q18, for a -3.0% swing.

This is the major reason we would downplay the growth in consumer spending. For most of the last five years, consumer demand has grown nicely, but much or most of that growth has gone to imports. This changed starting in 2Q17 and through 2Q18, when the drags from trade waned then turned into a large 2Q18 boost. With the deterioration in 3Q18, the trade balance is all the way back to the declining trend that had been in place through early-2017.

Whether the recent deterioration in trade is a result of Mr. Trump’s trade war or merely a reversion to trend following a (spurious) swing in previous quarters is a great question. The more relevant question is how trade will "flow" going forward.

That is, despite better capital spending and sporadically better consumption seen lately, the main factor boosting GDP has been the improvement in foreign trade relative to previous trends. If those adverse "previous" trends are back in place, it will be awfully hard for GDP growth to sustain anything better than 2.0%-2.5% growth. Inventories propped up growth in 3Q18, but it is hard to see inventories contributing thus going forward.

Meanwhile, GDP deflator inflation is back at the 1.5% plus/minus rate holding prior to the recent oil price bounce. We think that can continue.