The surprises were in the smaller, more volatile components such as the trade balance, equipment investment and inventories. Non-auto equipment investment was up at a nice 5.0% annualized rate, after having shown essentially zero growth for the previous two years. The trade balance was down sharply from 3Q16, though not as sharply as was expected.

The biggest upside surprise within the data came from inventories, which served to boost headline GDP growth by a full percentage point in 4Q16, after having provided a 0.5% boost in 3Q16. An inventory contraction had pulled down headline GDP growth in late-2015 and early-2016, but that has been largely reversed in the last six months according to the GDP data.

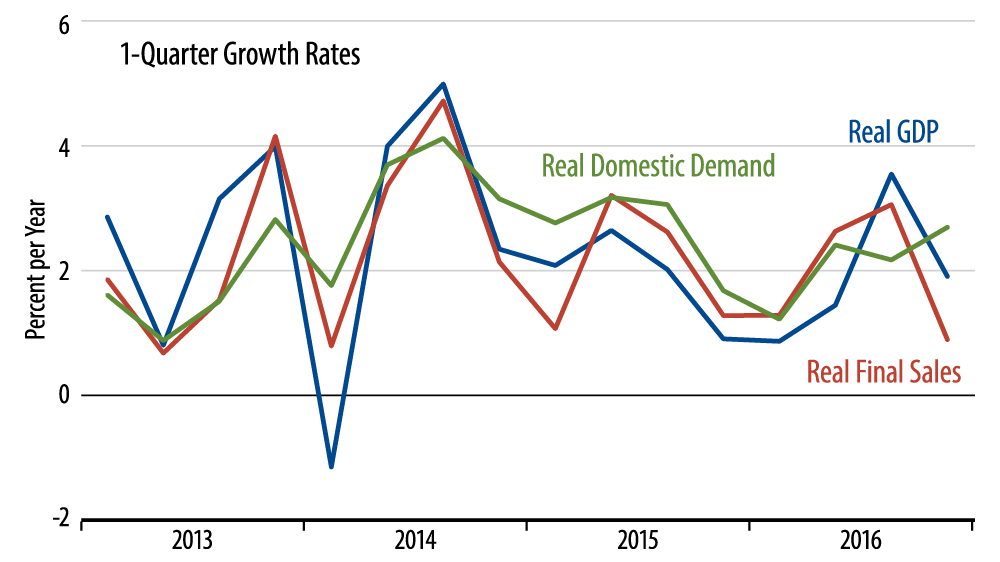

With growth tepid, inventories up strongly and the trade deficit down sharply, 4Q16 growth was clearly a convoluted story. The chart summarizes the conflicting currents within the data. Headline real GDP growth pulled back toward the sluggish trends of the previous year-and-a-half. Growth in real final sales (red line), which excludes inventories, grew at a slight 0.9% rate in 4Q16, but real domestic demand (green line), which excludes (declining) exports and includes (rising) imports, grew at a nice 2.7% rate. Clearly, both bulls and bears will find something to harp on within these data.

Current estimates have growth for the full year at 1.9%, the same as in 4Q16 itself. Going forward, GDP growth rates will be largely influenced by those swing factors, foreign trade and inventories. If the inventory rebound peters out and imports continue to grow, GDP growth in early-2017 will come in soft. If inventories can continue to move higher and imports flatten out, GDP growth could accelerate the way the market and Trump voters/investors are expecting.