It is widely perceived that economic growth has slowed in the last few months, a major factor behind the Federal Reserve’s decision to pause its rate hike operations. The issue has been how much growth had slowed and whether that deceleration would continue and threaten recession. Today’s news should allay the latter fears...for a while at least.

In the last few weeks, the economic indicators released by the government had become quite chaotic. After a very strong November gain, retail sales showed an even stronger December decline. Foreign trade data showed a sharp improvement in the trade deficit in November, following months of steady deterioration. Finally, wholesale trade data had shown a very sharp November increase in wholesale inventories. It does not appear that any of these swings were reflected in the 4Q18 GDP data.

That is, real consumer spending on goods was estimated to have grown at a 3.9% annualized rate in 4Q18, even though the retail sales data suggested a rise of only 1.0%. Similarly, the November data suggested that foreign trade would provide a good-sized boost to 4Q18 growth. Instead, the Commerce Department estimated trade to have been a drag on 4Q18 growth. Similarly, rather than a substantial boost to growth, Commerce reported inventory investment to have been a drag.

It is too early to know for sure, we’ll have to examine the GDP and related data in more detail, but it could be that retail sales, foreign trade, and wholesale trade data will all see substantial revisions to recent prints. Commerce has been adamant that the government shutdown did not result in any distortions to its data announcements of the last month. However, judging from the apparent discrepancies between the details of those reports and what was reflected in today’s 4Q18 GDP data, that statement is hard to credit.

As expected, the GDP data did show declines in business equipment investment and housing construction. However, those declines were not sharp enough to prevent a decent growth report for 4Q18.

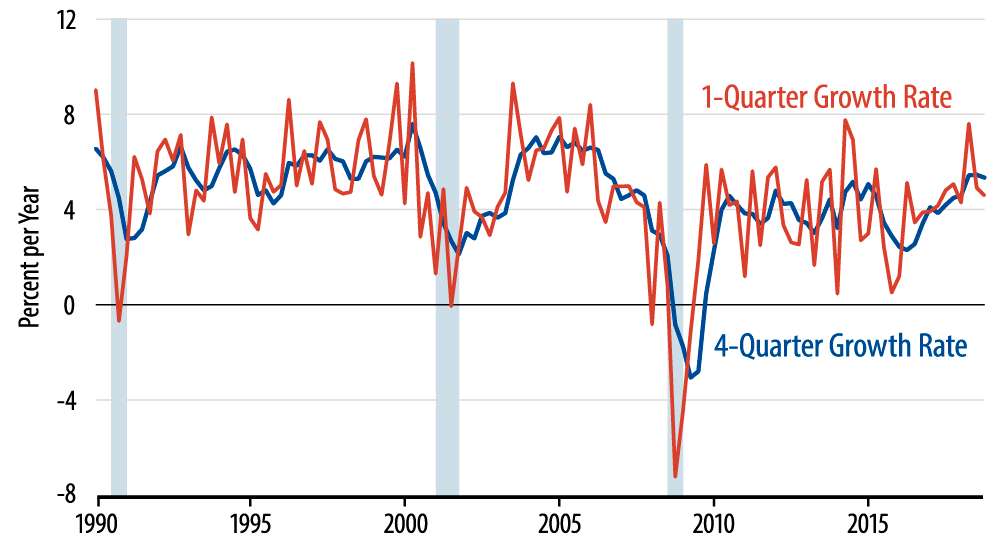

Finally, the combination of slower growth and reduced inflation resulted in noticeably slower growth in nominal GDP. As seen in the accompanying chart, growth in nominal GDP has pulled back to the trend rates of the last 10 years, after a brief bounce in late-2017 and early-2018. The slow and steady growth in nominal GDP in this expansion signals to us that Federal Reserve policy has had only moderate effects on the economy and that, therefore, a sustained acceleration in inflation was not in the cards. The recent reversion to trend in nominal GDP growth lends further support to that assertion.