2014年5月27日時点

Durable goods orders data provide information on both the manufacturing sector and on capital goods spending. Both manufacturing in general and CAPEX in particular are widely expected to be important drivers of stronger US growth this year.

Today’s data indicate soft growth in April in both capital goods orders (excluding aircraft) and durable goods orders in total, with the former down -1.2% and the latter up only +0.1%. However, both saw upward revisions to March data. Meanwhile, both were weak in January and February, so some of the more recent “elevation” may be catch-up from downward-distorted winter data.

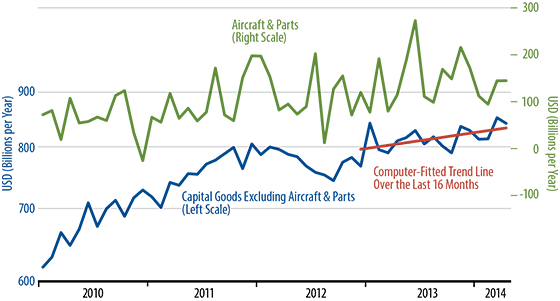

The chart below shows CAPEX orders. The red line shows a computer-fitted trend line over the last 16 months. This trend is consistent with 3.5% annual growth in core CAPEX orders (“core” CAPEX orders exclude aircraft and parts).

+3.5% is better than the zero-growth trend that seemed to have characterized this series at various times over the last year. However, it is far from robust growth and is even much slower than what was seen in 2010 and 2011. (Note also that total CAPEX growth is even slower, thanks to recent zero-growth trends in aircraft.) Furthermore, this 3.5% trend now looks to have been in place since late-2012, so it is no impetus at all to faster GDP growth this year.

Much the same can be said of durables orders in general, which have exhibited a 3.3% per year growth trend over the past 18 months. Durables activity and CAPEX are growing, but probably not enough to make a difference for the overall economy.