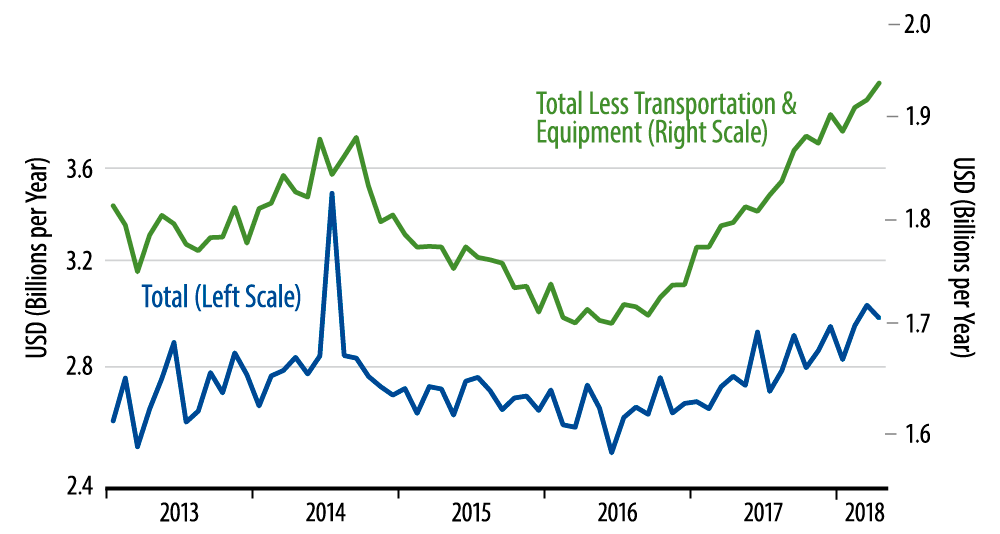

It can get confusing for readers when we economists parse the data, always taking out select components. However, this process, when done right, is intended to abstract from short-term noise and better portray underlying trends. For durable goods manufacturing, transportation equipment orders are especially volatile, thanks to aircraft orders which regularly swing by 50% from one month to the next. And, as you can see in the accompanying chart, durables orders ex aircraft do indeed show much smoother, more reliable movements than do durables orders total.

Now, even with their April increase, durables orders ex transportation show somewhat slower growth for 2018 to date than they did across 2017 (a 5.2% annualized rate over January–April 2018, compared to 9.7% for all of 2017). This is probably just a random fluctuation, but we will monitor it to see if the slower growth so far this year is indeed for real.

Benchmark revisions were also released for the orders data. These show much softer performance through late-2016 than previously reported, but about the same growth rates for 2017.

Concerning capital spending, new orders for capital equipment (also ex transportation) rose 1.1% in April. For this aggregate, benchmark revisions showed softer growth in 2016, but more steady growth trend recently. This actually works to clear up a mystery. The previous data had shown CAPEX orders starting to rise in mid-2016, then going flat over the last six months. This was odd given that that the recent flatness in CAPEX orders coincided with passage of the corporate tax cuts, which should have worked to spur investment. The revised data, however, now show CAPEX orders flat until November 2016, then growing at a reasonably stable pace across 2017 and recently. In other words, investment activity now looks to have perked up just after the 2016 election, when expectations of a more favorable investment environment emerged, and continued to grow recently, when those expectations became reality.

And if you suspect partisan tampering with the data, don't. The revisions to the orders data mirror similar revisions the Federal Reserve has made to its estimates of manufacturing output.