2014年5月16日時点

The decline in bond yields this year has astonished many observers. Proffered reasons for the decline range from events in Ukraine to US pension derisking, but a dominant undercurrent driving yields lower clearly is the US economy's failure to launch. And a prominent aspect of that failure is the ongoing stall in homebuilding.

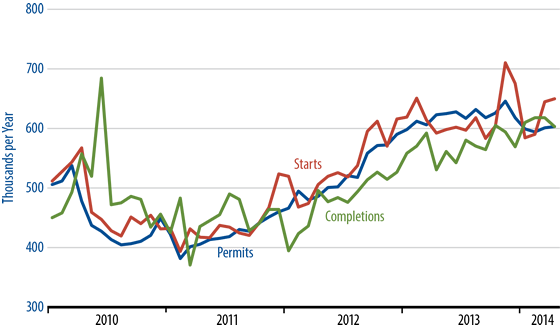

This brings us to today's news. The Census Bureau reported a slight gain in April, single-family housing starts following a more substantial increase in March. This leaves starts levels below late-2013 highs, but somewhat above the prevailing levels of the last 18 months. Meanwhile, trends in single-family permits and completions remain dead steady, somewhat below the recent prints for starts.

Multi-family activity drove a much larger gain in total housing starts. However, multi-family starts are extremely volatile month-to-month, and multi-family construction spending is a pittance compared to single-family.

All in all, these data are a "push" or at most a small hit to the bond markets. The steadiness of all single-family homebuilding indicators should preempt fears of a housing decline. At the same time, there is little indication of an impending move steadily higher, and a steady ascent is necessary if GDP growth is to accelerate and yields are to rise.

Meanwhile, other measures continue to suggest that the net housing demand we are seeing is coming primarily from investors, not from "grass roots" owner-occupants. The number of owner-occupied homes continues to slide, as it has since 2006, and household formation continues to proceed more slowly than growth in the adult population; each of these is a sign of lingering effects of the 2008 trauma. The existence of investor demand is clearly a positive, but without grass roots support, the upside for homebuilding is limited.