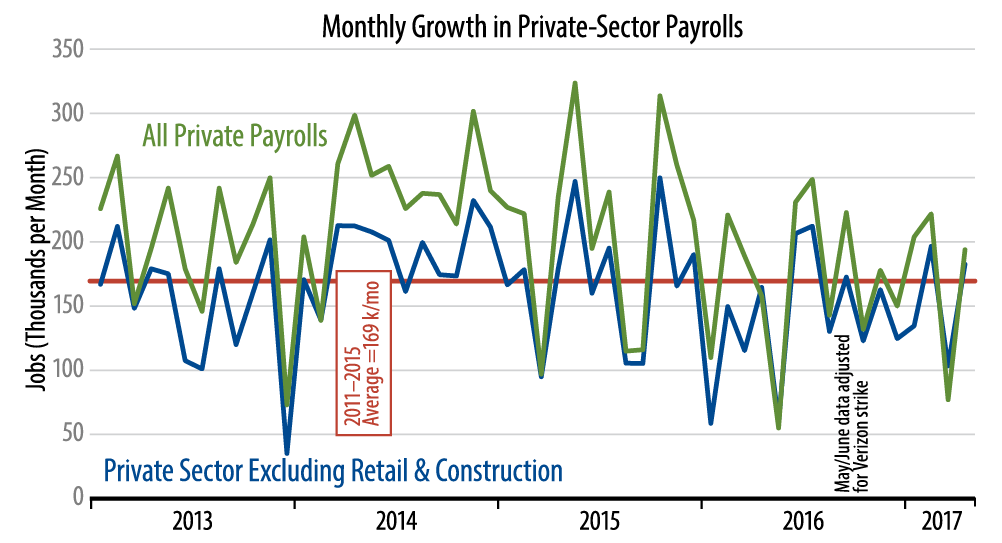

With a really weak month followed by a better growth month, it is sensible to average the two months together. For the last two months, private-sector job growth averaged 143,000 per month, while our preferred measure saw average growth of 135,000. The latter is well below the 169,000 per month average we were seeing through the end of 2015. As the accompanying chart shows, job growth has been slowing for the past 15 months, and the last two months—together—continue that trend.

We have been emphasizing this point recently. The consensus view is that the slower, recent job growth is okay, because that is all we need to sustain full employment. At the same time, however, the consensus claim is that economic growth is picking up. How can you have overall economic growth picking up while job growth is slowing? You can’t.

So, whether or not recent job gains are consistent with full employment, they are clearly not consistent with accelerating economic growth. And with no acceleration in growth, it will be hard to sustain the increase in bond yields and stock prices that we have seen over the past eight months.

In terms of sector details, both retailing and construction have seen slower net job growth recently, retailing over the last seven months, construction over the last two. So, if anything, the ex construction and retailing measure we track portrays a more “constructive” picture than do the headline data.

Manufacturing payrolls had stumbled in March, but we saw a modest rebound in both factory production jobs and workweeks in April, so that gives hope that the factory rebound of the last five months is continuing. Overall, again, the April jobs report was decent, but it wasn’t as good as March’s news was bad.