Recall that the strong March gains came after a sales plunge in December that was only mildly offset in January and February. So, the large March increases were merely enough to offset the December decline and impart some upward drift to sales levels. With April sales weak, the downside appearances for retail trends resurface.

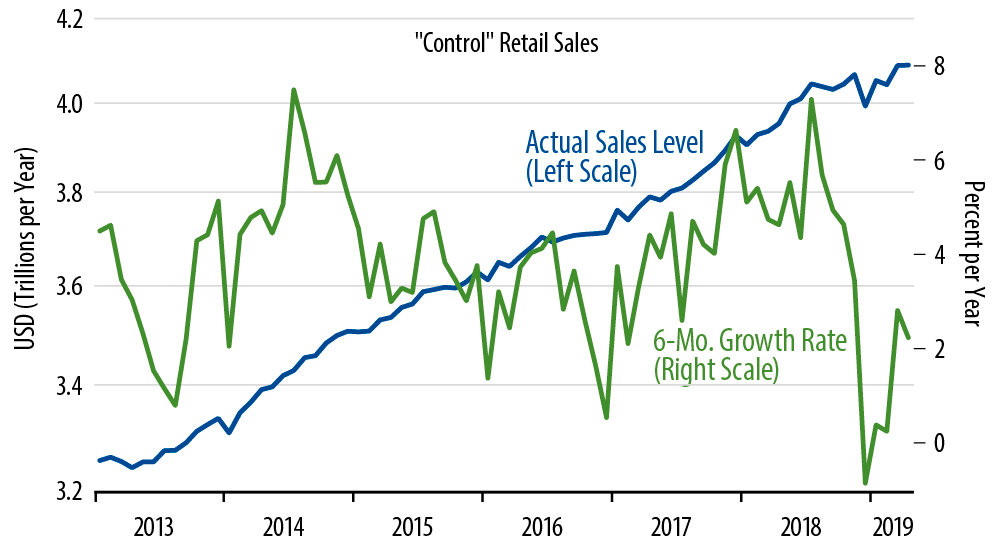

The accompanying chart shows monthly levels and six-month growth rates for our control sales measure. As you can see there, net of all the recent ups and downs, sales gains over the last nine months have been noticeably slower than preceding trends, and this is mirrored by the six-month growth rate, which has been hovering around 2.0% for the last few months, down from 3.5% or higher growth earlier.

The U.S. Census Bureau releases typically caution that it takes a number of months to establish a change in trend. We have now had nine months of net slower sales growth, and that should be a sufficient sample size to conclude that consumer spending on goods has downshifted a bit.

Lest you heed the various doomsayers that no doubt will pounce on this evidence, we’ll throw out a few countervailing points. First, retail sales cover consumer spending on merchandise. Services account for a larger share of consumer spending (about 60%), and they show no such slowing in recent months. Similarly, regardless of whether retail sales are growing strongly or weakly, much or most of that spending these days goes to imported goods, so the net impact on US economic growth is much smaller than the retail trends might suggest.

Having said all that, we were looking for substantially slower economic growth this year even with an expectation of steady growth in retail sales and goods consumption. Our guess has been for 2.0%-2.25% growth. The clearly slower retail sales growth of recent months adds some slight downside risk to that forecast, say now to growth in the 1.75%-2.0% range. Compare this to the 3.0% average growth of 2018, throw in the recent deceleration in inflation as well as the threat of yield curve inversion, and you may well get a recipe for some insurance cuts from the Fed.