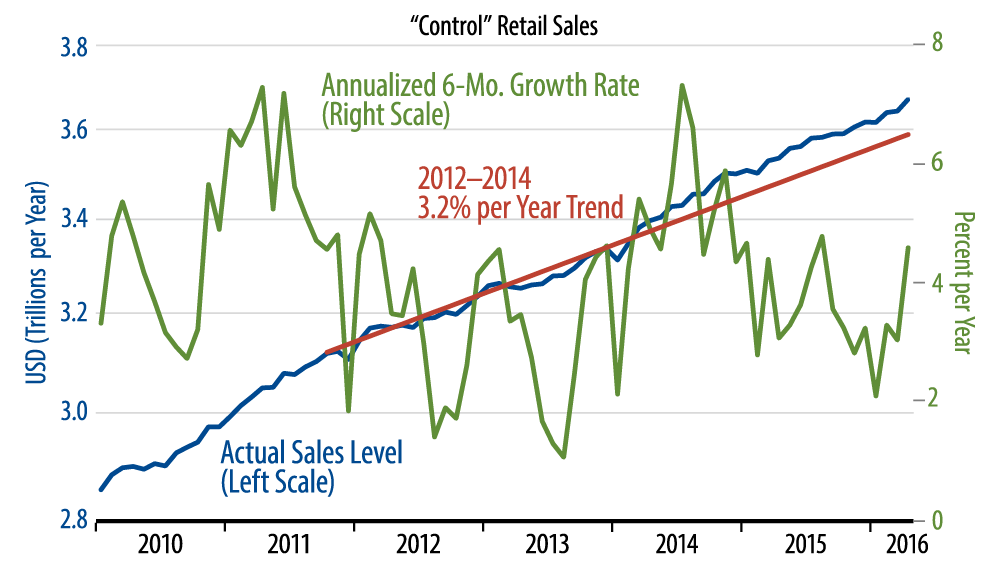

Retail sales grew nicely in April, with headline sales up 1.3%, and the "control" measure we track up 0.8%, on top of a 0.3% upward revision to March sales levels. The data are summarized in the accompanying chart.

As seen there, after rising above trend in late-2014, underlying sales levels had been moving back toward trend over the past year, with the last 3 months of data looking especially lackluster. Then along came today's better report.

On the heels of 3 consecutive soggy sales months, a softer headline jobs number and glum reports from major retailers, there was concern across the markets for retailing heading into today's data. Presumably, the better results announced today will dispel some of that gloom.

No, the consumer is not tanking. Consumer spending growth is not accelerating so as to offset the drags from capital spending and exports, but it is holding steady, rather than piling onto those drags. All in all, we think the data remain consistent with GDP growth in the mid-1% range, with little downside or upside risks around that rate.

The details within the retail report were a bit less spectacular. Auto sales were up a nice 3.2% in April, charging the headline gain, but that merely offset a -3.2% print in March. In other words, on net, auto sales have still gone flat over the past 7 months. There were similar gains in April sales at electronics stores, offsetting similar declines in late-2015 and leaving sales there still down substantially from 2015 levels.

The clear winners in the report were "nonstore retailers," mostly online vendors. Their sales rose 2.1% in April, on top of steady gains in previous months. These gains were the main driver behind the April pickup in control sales.

On the one hand, this indicates that consumer spending overall is growing okay. On the other hand, it suggests little support for traditional brick-and-mortar store expansion. I'm sorry to sound like the proverbial two-handed economist, but once in a while, the shoe fits...even when you buy it online.