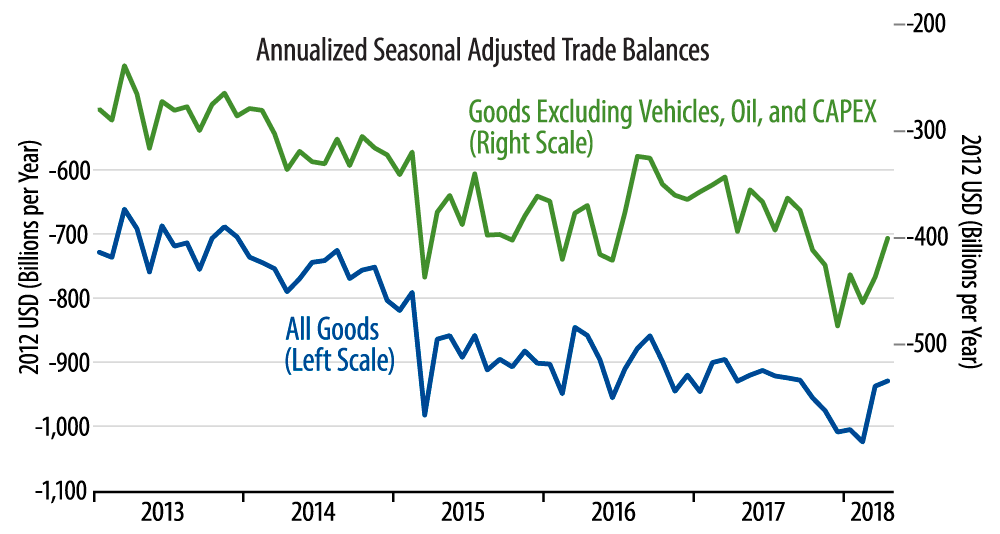

The chart shows the trade balance in inflation-adjusted terms, both total and excluding selected components. Both of these measures also show marked improvement over the last two months, driven by increases in exports and declines in imports. Prior to the March swing, export growth had been listless, while imports had been rising steadily, driving a steady deterioration in the trade balance. This, in turn, had been an ongoing drag on GDP growth.

The sudden reversal of fortune for trade has meaningful implications for domestic growth. The March swing in trade single-handedly boosted 1Q18 GDP growth by a full percentage point. If trade continues through June at the pace of the last few months, that would be a big boost to 2Q18 GDP growth.

What’s caused the sudden turns in both exports and imports? Great question! Growth abroad has appeared to slow in recent months alongside widespread claims that US domestic demand is heating up, while the dollar has strengthened and fears of a trade war have arisen—not an auspicious climate for US imports to suddenly stagger and US exports to suddenly surge. The March/April data, however, suggest that this is exactly what happened.

As demonstrated in the chart, the trade balance has taken a number of contra-trend turns over the last few years, only for the downtrend in the trade balance to eventually reassert itself. We’ll see in coming months whether that happens yet again. In the meantime, the recent improvement in the foreign trade picture is a challenge to our below-consensus growth forecast. As we’ve written, we don’t see any recent acceleration in consumer spending, and domestic capital investment may have downshifted a bit recently. So, in our view at least, the last two months’ turnaround in foreign trade is the one piece of news supporting a stronger growth story.