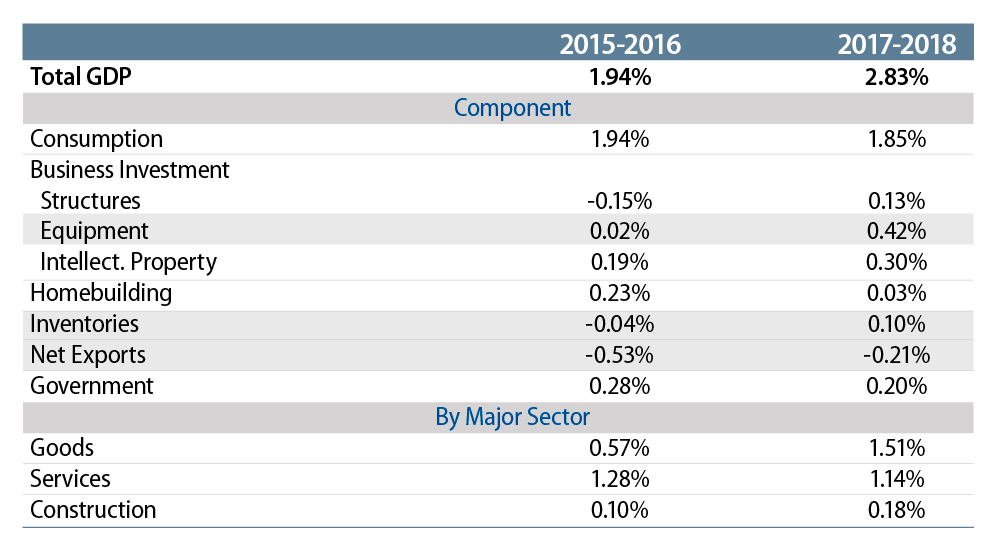

While 3- and 4-handle growth in some recent quarters has garnered headlines, average growth for all of 2017-18 is a more modest 2.8%, albeit still up from 1.9% over 2015-16. As the table shows, all of this improvement has come in only a few GDP areas.

Notably and contrary to popular perception, consumer spending has grown no more rapidly over 2017-18 than it did over 2015-16, contributing 1.9% to average growth in both periods. In contrast, all the 0.9% pickup in GDP growth can be accounted for by foreign trade (net exports), inventories and equipment investment. And each of these face "issues" heading into 2019.

Foreign trade flows benefitted from sporadic jumps in exports and declines in imports in both mid-2017 and early-2018, apparently in anticipation of a trade war. Trade trends have reverted to pre-2017 trends recently, and we expect trade to provide just as much drag on growth in 2019 as it did in 2015-16, especially with trade policies restraining growth.

Given the 2017 tax bill’s incentives, one would think capital spending would continue to hum, but recent capital goods data have been spotty. Meanwhile, homebuilding looks to have embarked on a downtrend. If foreign trade and inventories do indeed revert to 2015-16 trends and either equipment investment or housing sputter, economic growth could drop to the 2.0%-2.25% range.

(One could coax a higher recent growth number by looking at the last six quarters rather than the last seven, that is, by excluding the 1.8% growth seen in 1Q17. However, that 1Q17 growth reflected blizzard effects that were reversed in 2Q17, so the two quarters should be taken together.)

As you can see in the lower part of the table, all the 2017-18 growth acceleration came in goods-producing sectors, particularly manufacturing and mining. Services and construction—the other 71% of GDP—showed no improvement. So, as nice as the economy’s performance has been since early-2017, that improvement has been narrowly focused. It is good to see US manufacturing growing again, but this growth cannot be taken for granted. Meanwhile, it is not clear whether US oil output (mining) can continue to grow at its recent pace.

We think the claims of runaway growth are exaggerated and that we will likely see more modest performance in 2019, along with continued low inflation. This combination is likely to stay the Fed’s hand relative to the hiking intentions it has already announced.