2015年09月04日時点

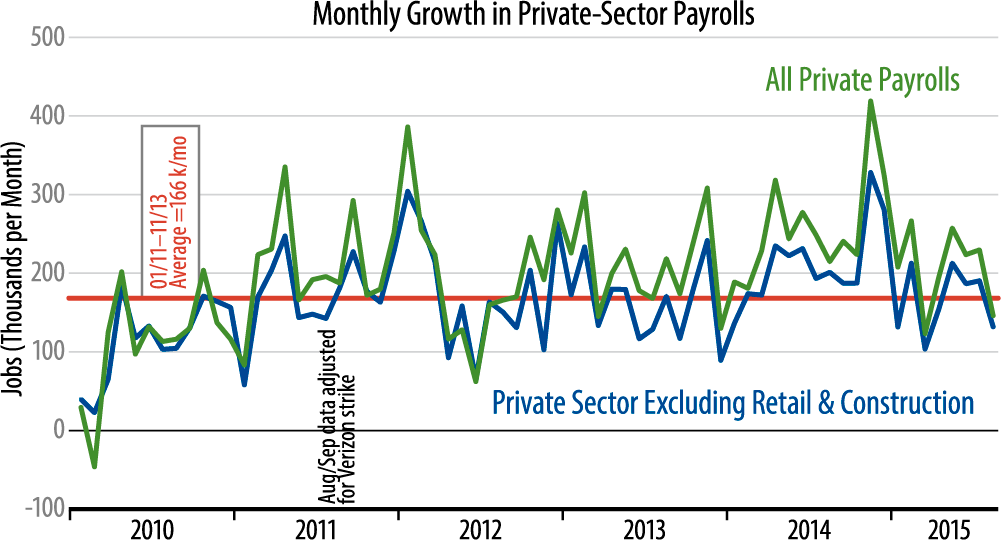

Payroll job growth is reported to have slowed in August, with private-sector jobs rising by only 140,000 and only slight revisions—up 5,000—to the July total. The “core” measure we track rose by 126,000, with a 7,000 upward revision. As can be seen in the accompanying chart, the August gains are well below the average growth rates of the past few years.

There were widespread reports looking for a weak number, based on the fact that past August jobs reports had typically been revised upward by some 50,000 or more jobs. Thus, various analysts are actually seeing today’s report as a positive one, thanks to “only” a 50,000 or so slowing in job growth, slight gains in workweeks, and better gains in hourly wages. A little averaging out puts the doubt to such claims.

As seen in the chart, today’s data give us the third report this year showing well-below average job gains, and the below-average months look more pronounced than the above-average ones. Similarly, the better data on workweeks and hourly wages are offset by below-average prints for these series in previous months.

Additionally, while household jobs data were touted today as rising a “strong” 194,000 in August, that comes after total gains in June and July of only 45,000. It is an overstatement to say that job growth is weak or weakening. Still, claims that today’s report is a strong one are strained.

Meanwhile, we have paid special attention here to the manufacturing sector and thus to factory payrolls with the jobs report. There, factory payrolls had stabilized in early summer, following steady, substantial declines in early-2015. The August data signal a reversion to early-2015 downtrends, with factory production payrolls down 30,000 in August, with previous months’ levels revised downward, and with factory production hours dropping 0.4% in August, this suggests yet another drop in industrial production.

The overall job gains may well be enough to induce a Fed rate hike this month. The more important issue is whether Fed actions will be forceful enough to induce upward movement in note and bond yields. Our reading of the data suggests not.