None of these numbers are spectacular, but each of them continues a pattern of growth that has been in place for over a year now. Both capital spending in particular and manufacturing activity in general had shown zero growth—actually some declines—from early-2012 through the middle of 2016, but both have been rising fairly steadily ever since.

Our take on the overall economy is heavily driven by developments within manufacturing. Though only a slight share of total employment, the factory sector accounts for the lion’s share of swings in overall economic growth, so the renewed growth in manufacturing activity over the past year has been a welcome change.

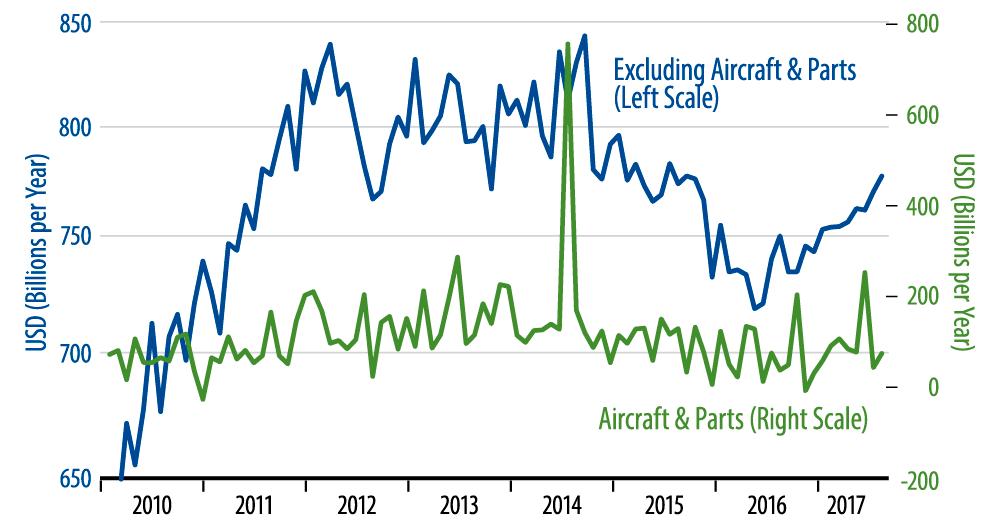

The factory sector rebound in late-2016 was driven by renewed gains in both capital spending and exports. Exports stalled out around the beginning of 2017, but capital spending has continued to grow, and, lately, the gains there have been accompanied by inventory rebuilding.

Inventory rebuilding runs don’t go on forever, and we have some concerns that a factory sector rebound driven by capital spending alone will be uneven and tenuous. For now, though, those concerns seem to be whistling in the wind. Overall factory payrolls are growing nicely recently, and so are factory orders and production. Though hurricane effects will likely distort the factory sector data in the next two months, overall manufacturing trends are the best we have seen since the outset of the expansion.