For example, orders for capital goods excluding transportation equipment were announced as up 0.6% in August, but there was a 0.7% downward revision to July. Similarly, orders for all durables excluding transportation equipment were down 0.4% on top of a 0.2% downward revision to July. No sector was down sharply including revisions, but the lack of any substantive gains left the prevailing downtrends in manufacturing intact.

Continuing factory-sector weakness has been the main driver of our near-term economic forecast. It has been the dominant factor driving slower GDP growth over the past year, slower job growth in 2016 to date and even declining corporate profits over the last two years. Our analysis indicates that this weakness in manufacturing has been in place since early-2012, nearly five years now.

The consensus line has been that the factory stall is a recent phenomenon that will turn around soon. So when factory data turned a bit better in June and July, it keyed widespread calls for a sustained upturn there and therefore better GDP growth in the second half of 2016.

The data released this month have rained on that parade. Factory payrolls, industrial production and now durables/capital goods orders all have shown downward revisions to July data and further softness in August, thus sustaining ongoing downtrends for these measures.

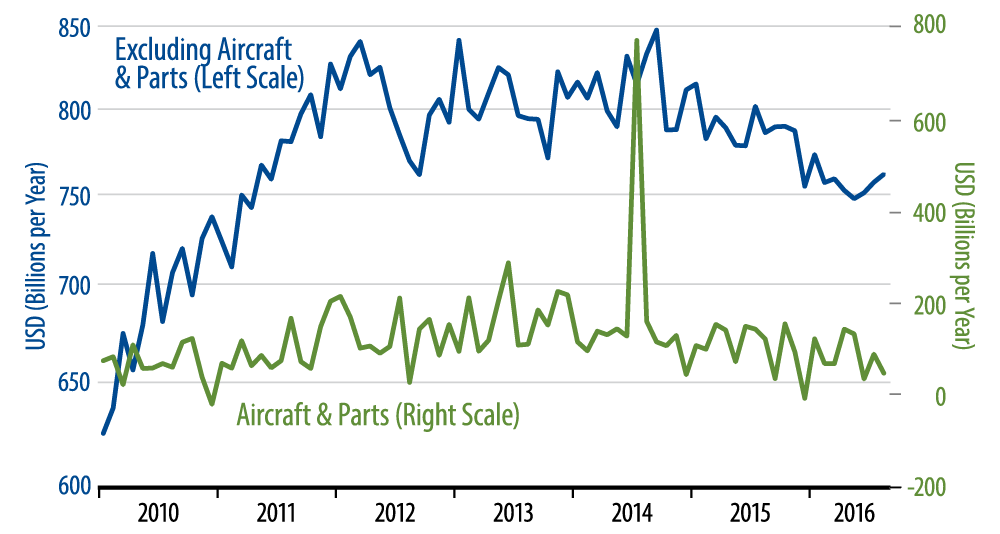

The capital goods orders data plotted here are actually the “pick of the litter” for manufacturing indicators. You can see some gain in CapEx orders over July and August, but not enough to reverse the soft trends that have been in place for this indicator since early-2012. Data for factory payrolls, industrial production and overall durables orders fail to show even such a muted recent bounce.

We look for continued softness in manufacturing and, consequently, continued 1-handle GDP growth at least through the end of this year.