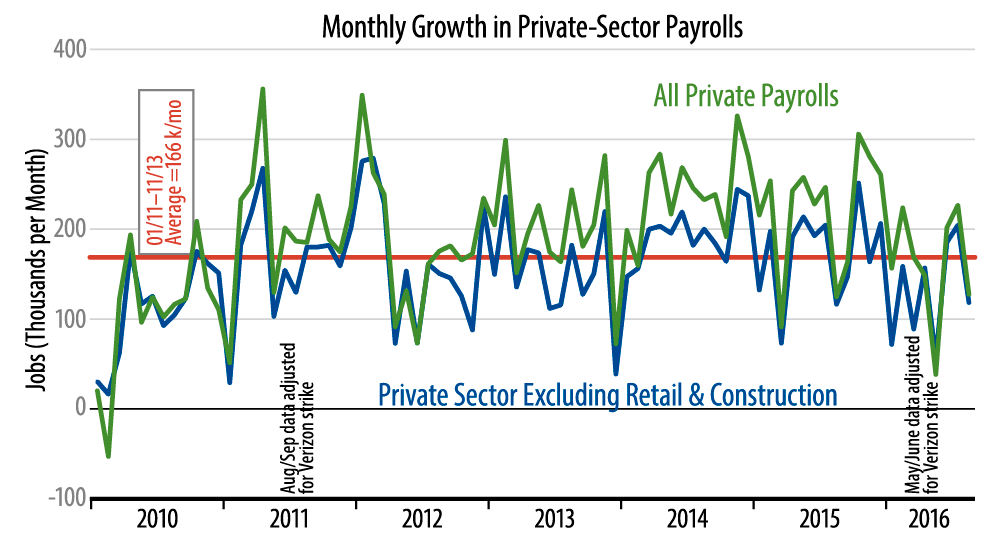

Private-sector payrolls disappointed in August, adding 126,000 alongside a downward revision of 13,000 to July data. The core jobs measure we track, excluding retailing and construction, rose by 117,000, with July’s number unrevised. The August data resumed a year-long trend of slower growth, following stronger prints in June and July.

The accompanying chart tells the story. No, job growth is not imploding, but there has been a clear deceleration in growth this year, reflecting the even sharper deceleration in GDP growth (from 2.0% to 2.5% over 2011 through early-2015 to 1.2% in the last year). The cause of both these decelerations is clear: a major slowdown in the US factory sector. Goods-sector GDP grew a scant 0.5% in the past year, compared with a 4% growth trend over 2012–2014. Similarly, the slower job growth this year is entirely due to declines in manufacturing jobs, as well as in the industries upstream and downstream from manufacturing: mining and logistics.

In line with these trends, factory payrolls resumed their downtrend in August, with factory production jobs down 13,000 in August. In addition, a -12,000 revision to July factory production jobs erased the previously announced gain for that month and more than offset the 8,000 gain in June that remains in the data.

Many analysts had been proclaiming a rebound in manufacturing, based on the June/July data. We were skeptical of this, given that the main drivers of factory weakness, capital spending and exports, had not shown any improvement that would presage a production upturn. Today’s data confirm this skepticism, with the downtrend in factory production jobs now firmly entrenched and similar developments likely with respect to factory output within the industrial production data. (Factory workweeks also declined substantially within today’s release.)

Our growth forecast has been well below the consensus and consequently, we have been expecting fewer Fed rate hikes than the Fed’s rhetoric would suggest. Today’s news is consistent with this expectation.