Isn’t that horrible for government workers? No, the early-summer data on government jobs looked quite distorted/overstated. Since public schools have started moving to year-round schooling, the Bureau of Labor Statistics has had trouble correctly seasonally adjusting public education jobs. These troubles appear to have led to the abnormally strong government job tallies over the last two months, which artificially boosted the headline numbers then, but which were reversed in today’s report.

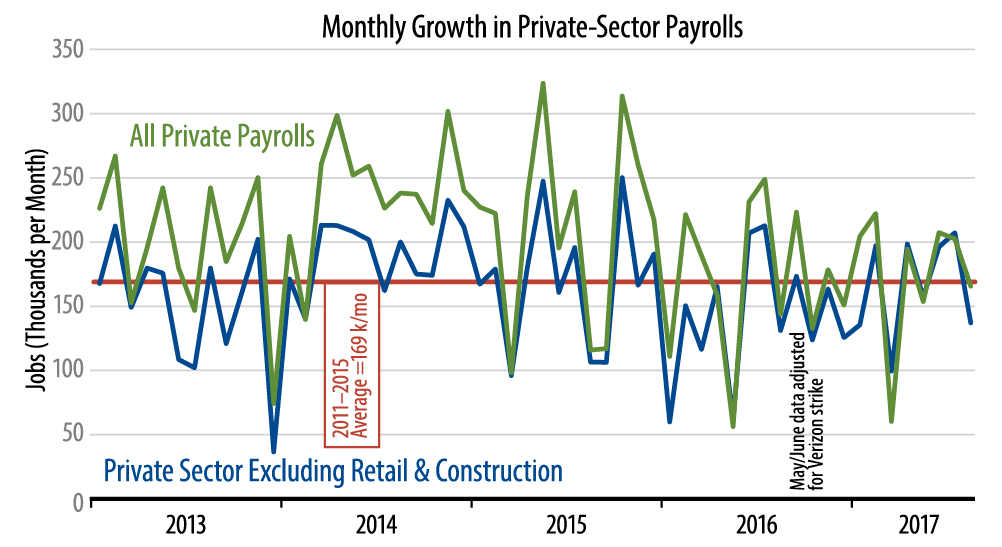

Away from the vagaries of government jobs, private-sector job growth looked more favorable. True, even net of government jobs, the August gains were a bit soggy, but that came after especially strong gains in June and July. As seen in the accompanying chart, the “core” jobs number we track, private-sector less construction and retailing, grew well above its 2011–15 trend rate in June and July, before falling to below-trend growth in August. On average, this indicator has grown by 169,000 jobs per month over the last seven months, right at the average growth rate seen through mid-2016.

Earlier this year, we made much of the fact that this measure had fallen below its trend path for much of late-2016 and early-2017. The performance of the last few months, however, has reversed that softening trend.

More importantly, to our eyes anyhow, is that factory jobs grew strongly in recent months. Factory production-worker jobs rose a whopping 50,000 in August, on top of a 27,000 gain in July. Manufacturing had looked to be stalling again through June, but it has come roaring back in the last two months.

Finally, the one truly soft spot in today’s news was hourly wages, which rose by only 0.1% in August and show growth of only about 2.5% over the last year.

Overall, the economy is displaying steady overall growth, with production growth tilting toward the goods sector and away from services, and no signs of higher inflation. This is a much brighter picture than we had been expecting.