2014年9月12日時点

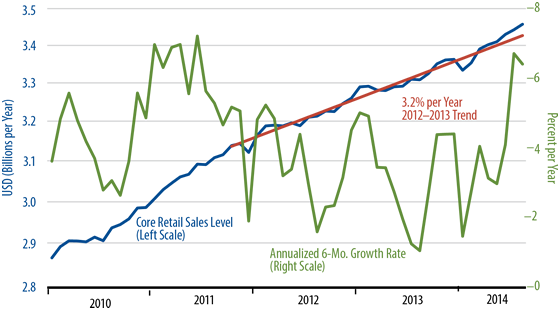

Today's retail sales data for August showed some decent gains—nothing spectacular, but a noticeable improvement from the steady trends of recent years. As we have remarked in previous editions of this commentary, retail demand in the spring rebounded just enough to offset the weakness induced by the polar vortex, but not enough to indicate any acceleration. Well, with upward revisions to the July data—from 0.1% to 0.4%—and a 0.4% gain in August, "control" retail sales now show a noticeable acceleration from the 3.2% per year growth trend that had been in place since the beginning of 2012 to 5.8% per year growth over the last three months.

The chart shows this acceleration, with recent sales levels rising above the 2012-14 trend line. No, the recent acceleration has not been dramatic, but it is noticeable. And no, one month's news does not by itself dramatically alter the landscape, but it does give one something to think about.

Our forecast line has been that the US economy was not accelerating and that growth would continue to fall below the Federal Reserve's forecast. Today's news is a strike against that line—a first strike, but a strike nonetheless.

In terms of store types, the Commerce Department figures indicate that sales gains remained sluggish. Vehicle sales were steady, while building-material store sales have continued to perk up since the winter. Among nondurables retailers, sales have been steady at grocery stores, restaurants and apparel stores, while department and big box store sales have leveled off lately after a strong spring rebound. There have been noteworthy recent gains at health care stores and "miscellaneous" retailers, which include office supply stores. Service station sales were off in reflection of lower gas prices.