2015年10月06日時点

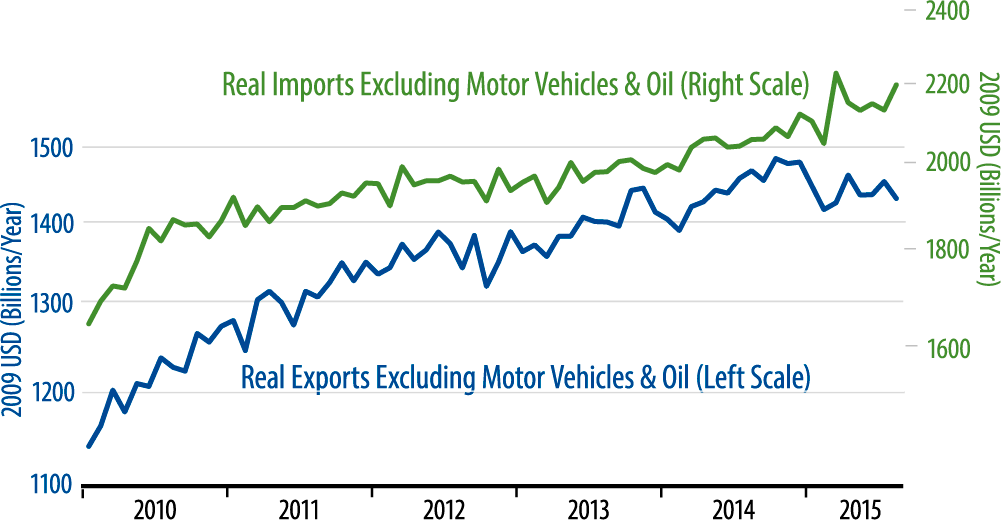

The US merchandise foreign trade deficit showed a sharp deterioration in August, on falling exports and sharply rising imports. In nominal terms, the merchandise trade deficit rose from $59.3 billion per month in July to $66.6 billion per month in August. In “real” terms, upon adjustment for inflation, this deficit rose from $56.1 billion to $63.4 billion (in 2009 dollars). Based on the August decline alone, it looks like merchandise foreign trade will subtract nearly a full percentage point from 3Q15 real GDP growth.

As adverse as these data are, they do provide some conformity between supply-side and demand-side data for US goods-producing sectors (which is why we focused on merchandise trade above, abstracting from services). Supply-side measures of goods-sector activity, such as manufacturing hours worked, manufacturing industrial production, and factory orders and shipments have all shown steadily negative growth since late-2014. On the demand side of the picture, the corresponding measure of goods GDP growth did indeed decline in 1Q15, but then it showed a strong increase in 2Q15.

There are valid differences between the two sets of data, because goods GDP also includes domestic value-added from shipping, wholesaling and retailing goods, activities that are not reflected in the supply-side measures. Still, it is all but impossible for goods GDP to continue to grow briskly if domestic production of goods is declining. The sharp increases in imports and sharp declines in exports in today’s data indicate that goods GDP will indeed decline within 3Q15 GDP data (to be released later this month), putting goods GDP data more into conformity with the supply-side measures listed above.

To put it another way, while the retail sales data indicate that US consumer spending on goods is growing nicely, the supply-side data (and foreign trade data) tell us that most of those goods are being produced abroad, thus providing only slight stimulus to the domestic economy. With at best sluggish growth in the goods-producing sectors, there is essentially no chance of a meaningful pickup in US growth, in which case our bet is that Federal Reserve tightening steps—when and as they come—will be cautious and halting, having little or no impact on the medium and long ends of the yield curve.