(Unlike other analysts, our control measure includes restaurant sales. Like other analysts, we exclude cars, gasoline, and building materials from control sales, because businesses engage in retail purchases of these items as heavily as consumers do, but we see no such reason to exclude restaurant sales.)

The January gains had looked strong when they were first announced a month ago, but later we found out that essentially all of these gains were due to price increases, so that real control retail sales actually declined by 0.2% in January. The revisions announced today will upgrade the January experience to a very slight gain in real terms. Then February follows with another slight gain.

When the real retail sales (and consumer spending) data were released two weeks ago, analysts chopped their 1Q17 GDP forecasts down on account of the weak showing. The upward revisions today will lead them to reverse some of that. However, the underlying message for consumer spending is still nondescript.

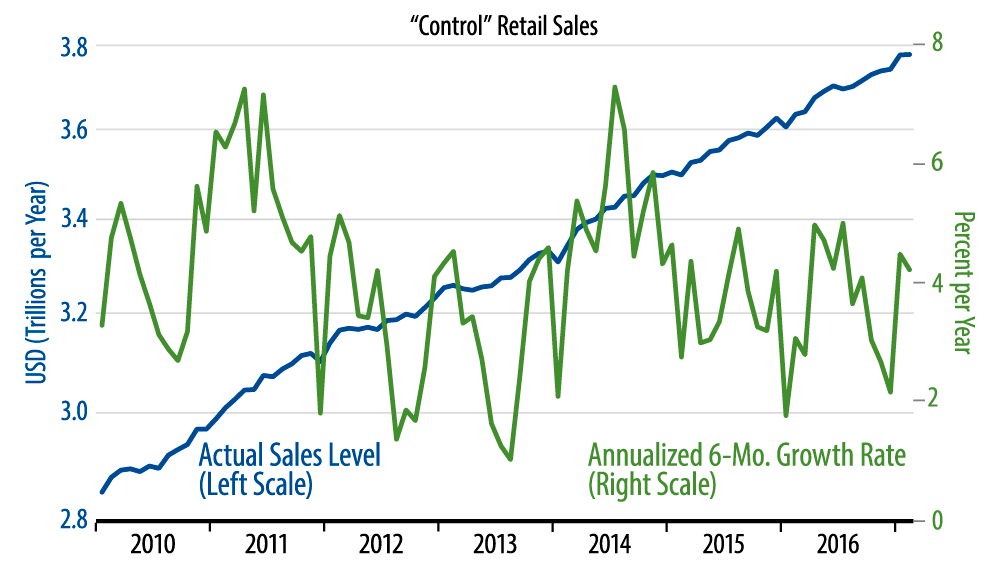

As seen in the accompanying chart, control sales trends are at best steady over the last eight months, and, again, the January price spike makes the real sales data even less impressive. Meanwhile, nearly 70% of consumer spending goes to services, which are generally not covered by the retail sales data, and these have also been sluggish in recent months.

Overall, the economy has looked a bit better in recent months, the manufacturing sector especially so. However, the consumer sector has not been a driver of this upturn. Rather, the main drivers look to be exports and inventories. Consumer spending is not weak, but neither is it showing any acceleration that would give further vitality to economic growth.