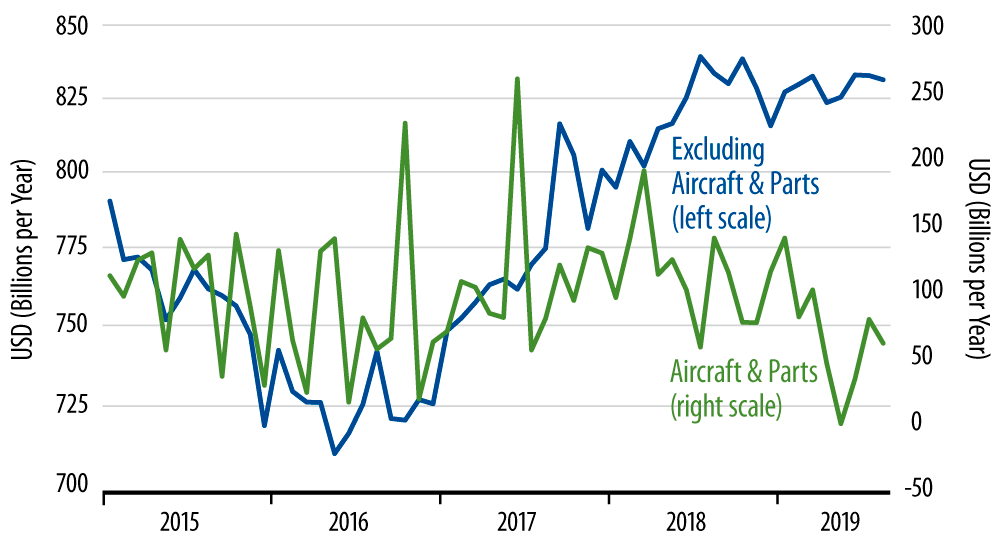

So, neither of the latter two indicators showed ringing gains in the summer, but both look to be maintaining a modest uptrend over the last four months, after having declined fairly steadily in the early months of 2019. Thus, durables orders ex transportation equipment show a +3.3% annualized rate of growth over the four months May 2019 through August 2019, compared to a -2.5% rate of decline over the preceding six months. Similarly, as shown in the chart here, capital goods orders ex aircraft have increased on net at a +2.9% annualized rate over the last four months, after having declined at a -3.6% rate in the preceding six months.

Neither one of these swings suggests an earthshaking rebound in the factory sector’s fortunes. However, together they do indicate a much better picture than what the "soft data," such as the Institute for Supply Management (ISM) Manufacturing Index, have been suggesting.

That is, the ISM index dropped below 50% in August, after having been above 50% over the first seven months of 2019. This movement suggested to some a sudden decline in factory activity in August.

In contrast, both durables orders in general and capital goods orders in particular had been declining since the summer of 2018 and, again, have been showing some rebound since April 2019. The inference for these measures is that factory softening began almost a year ago and has been moderating—or reversing recently. Similar readings have been given by other "hard data" indicators of manufacturing. Thus, factory production jobs, factory production hours worked, and industrial production by factories have all increased on net over the last four months after having declined steadily in the first four months of 2019.

In other words, rather than the recent weakening indicated by the soft data, the hard data show a softening that began as much as a year ago, but that appears to have turned the corner in recent months. The weakness in the soft data was a big part of the recession stories floating around early this month. Better economic data over the course of this month have quashed those recession fears somewhat, and we believe this is rightly so. Again, the yearlong softening in manufacturing has been a major factor in slowing overall economic growth this year from the headier pace of 2017-18. However, we have always contended that growth, while slower, was not weak nor weakening toward a recession pace. The modest but clear improvement in hard data for the manufacturing sector supports our position.