Our take coming into this year was that economic growth would slow from the headier pace of 2017-18, thanks to softer manufacturing-sector growth, driven by moderating exports and inventories, and to a softer homebuilding performance, as builders worked to cut back excessive inventories. However, we didn’t think that slowing would morph into any serious recession risk, and we pushed back early this year when slower growth signs were taken by some to imply recession risks.

Softer manufacturing and homebuilding activity has indeed occurred so far this year. In addition, early-2019 reports suggested some softening in retail sales, reflecting slower consumer goods spending growth, and when personal income data for late-2018 were revised sharply lower, we thought that apparently weaker income (and job?) growth was the reason for softer consumption growth. This additional source of slower growth still did not seem to us to constitute a recession risk, but it did bolster the case for some rate cuts by the Federal Reserve.

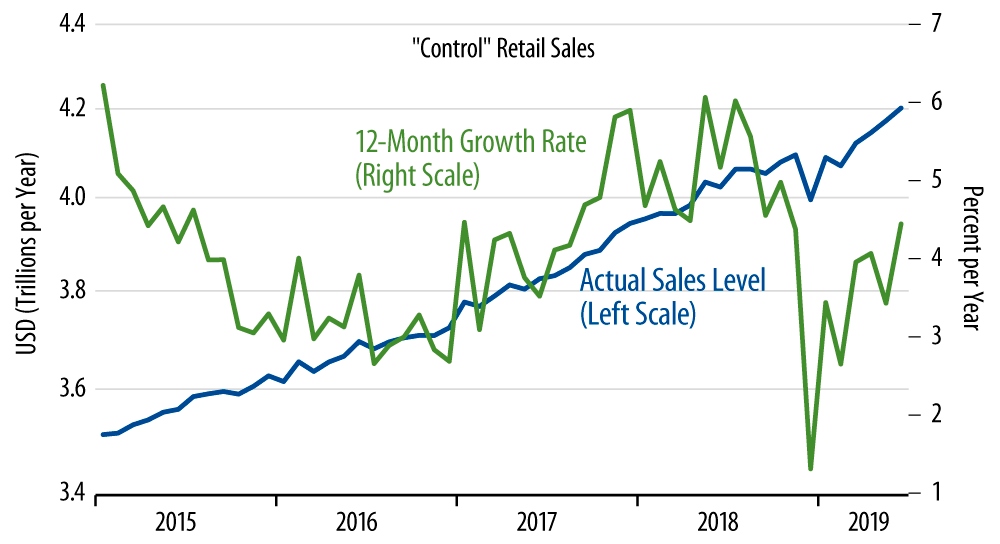

Recent months’ data have shown a better tone for retail sales. After a favorable May retail sales release analyzed in our June 14 By the Numbers, yesterday’s June retail sales release continued the more upbeat skein. The "control" sales measure we track—sales excluding cars, gasoline, and building materials—showed a robust 0.7% gain in June, with May levels essentially unrevised.

As you can see in the accompanying chart, the recent gains fully offset the softness that retail sales showed around the Christmas holiday. The 12-month growth rate for sales is now back to 4.4%, about the same as we saw in 2016-17, up from much slower numbers earlier this year.

Alas, the better performance of goods consumption has been offset by softer services consumption data. May data released late last month showed substantial downward revisions to services consumption in 1Q19, and recent months’ data indicate little or no growth for real consumption of services other than medical care. So, as suggested by the title here, the net story for consumer spending is little changed from what we were seeing two months ago, prior to the rebound in retail sales and goods consumption.

Meanwhile, just as the June jobs data perked up a bit, so too manufacturing output looks to have stabilized in today’s June industrial production report, following output declines over January-April. Data on homebuilding continues to be nondescript. Overall, we still see a US economy growing at a 2% rate or a little slower. We’ll comment further on this when the 2Q19 GDP data are released on July 26.