Meanwhile, the "swing factors" we excluded from the aggregates above were all weak in May. Vehicles and utilities spending both declined. Health care services spending has been flat throughout 2018 to date, after growing 2.5% in 2017.

Consensus economists have been expecting consumer spending to accelerate due to supposedly buoyant job growth and the tax cuts enacted earlier this year. We have been skeptical of this call, arguing that job growth has actually slowed and that the personal tax cuts are too meager to have a meaningful effect.

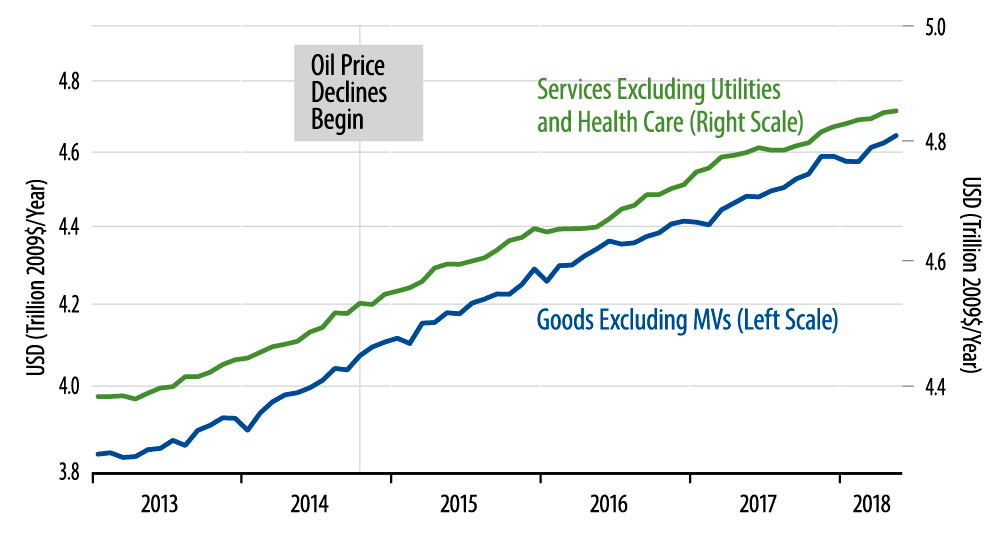

The admittedly strong retail sales report earlier this month seemed to be a confirmation of the consensus position. However, today’s full report on consumer spending indicates otherwise. As the chart makes clear, the May gains in consumer goods spending don’t really "move the needle" there. Meanwhile, if anything, services spending has slowed slightly this year. And keep in mind, again, that while choppy, the three elements excluded from this chart—vehicles, utilities, and health services—have all been flat or declining on net so far for 2018.

In other words, there is no real sign of the heralded consumer upturn. Personal income data also released this morning show decent growth, but at no faster a pace than has been seen in recent years. So, on the income side as well, we see no reason to expect stronger consumption growth. To be clear, consumption growth is not weak, but it is not accelerating in line with the consensus story.

This news comes amid proclamations of exceptionally strong 2Q18 GDP growth. It is worth noting that whatever acceleration in GDP growth occurs in 2Q18, it will be mostly due to an abrupt, dramatic swing in the US trade balance, with both imports suddenly dropping and exports suddenly surging. Who knows how long these swings will last?