Price gains were headed by relatively large gains for new cars (+0.3%), used cars (+1.3%), and airfares (+2.7%). Prices declined in both June and July for apparel, following earlier gains, and for medical care commodities, while medical care services prices rose "only" 0.1%.

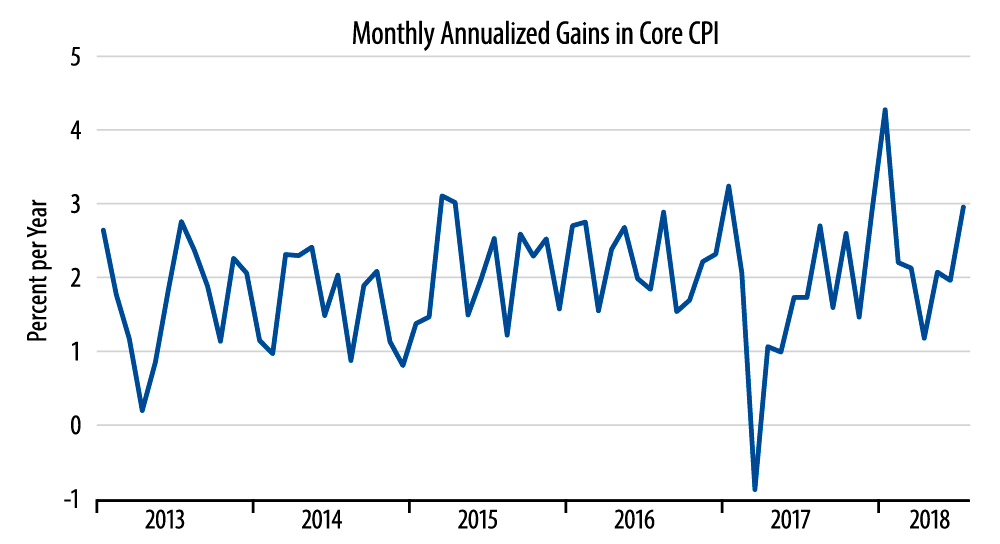

Last month, we pushed back against the consensus view that inflation was accelerating. We thought it more likely that CPI inflation was stable around a 2.0% trend. Apart from that aforementioned January spike, monthly inflation rates had not shown any sign of accelerating relative to the pace of the last few years.

(And, yes, a 12-month inflation rate was rising steadily, but that was occurring on the strength of that outsized January hike. In other words, other "filters" of the core CPI data did not exhibit an accelerating trend.)

As seen in the accompanying chart, the July price gains were above the general range of the past few years, though not by a lot. We would still argue that the assertion of accelerating inflation is far from clear in the data, but admittedly that assertion is a bit harder to push today than it was a month ago. As usual, we’ll have to see how subsequent data changes the picture, either toward or against our position.