Just to complicate matters a bit more, the Federal Reserve (Fed) tracks a measure called the core Personal Consumption Expenditure (PCE) deflator. It also estimates consumer prices excluding food and energy prices, but with a more reliable weighting system than what the core CPI uses (as well as other minor differences). The Fed has been calling for core PCE inflation to run to 2% or more this year. Through March, however, the core PCE 12-month rate had been 1.9%, and based on today’s CPI readings, it is likely that the 12-month core PCE inflation reading will drop to 1.8% in April.

We disagree with the Fed and market consensus on inflation. As detailed in a recent white paper, "Low Inflation is No Mystery," our position has been that neither Fed policy nor the movements in the economy were consistent with a sustained increase in inflation.

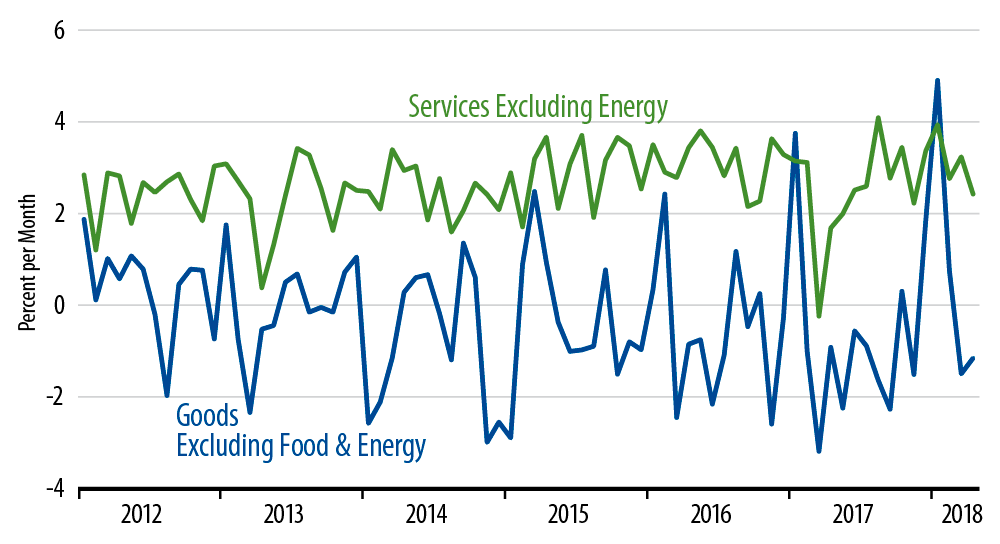

After a 0.3% core CPI reading in January, the "knives" were out among those looking for rising inflation. However, the readings of the last three months—and March and April especially—temper some of that fervor.

Even with the January inflation "spike," we were skeptical that inflation was taking off. After all, we had seen similar one-month spikes in January 2016 and January 2017, only for tamer inflation to resume in subsequent months. Similarly, as shown by the accompanying chart, the January 2018 inflation spike was centered in goods prices, like its antecedents in 2016 and 2017. Yet it is in the service sectors where economic performance has been better in recent years and where the inflation "bulls" were looking for price pressures to surface.

Instead, services inflation remained quite stable even through January, and now the last three months’ data have resumed the downtrend in goods prices. Today’s news doesn’t settle the inflation issue, but it should at least raise some eyebrows—and some questions—among those who are sure inflation is on the rise.