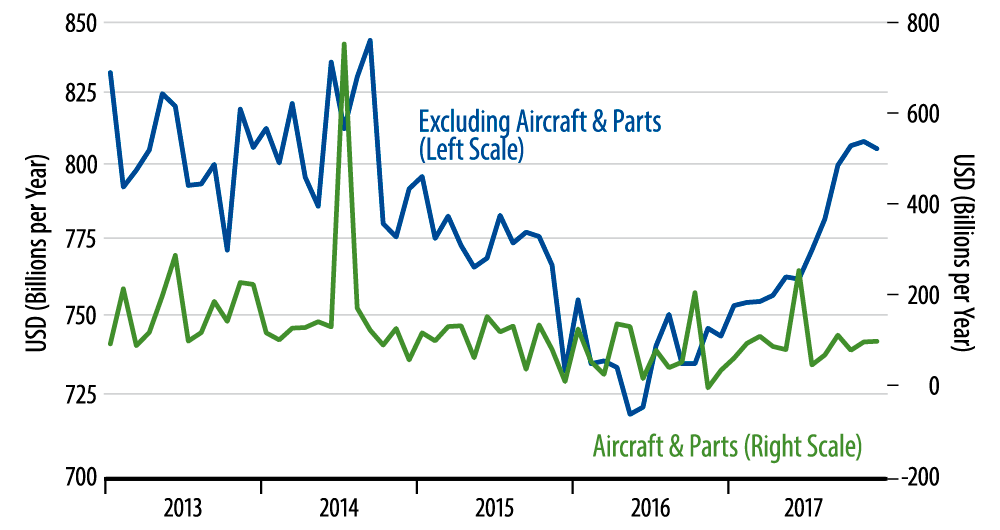

Overall durables orders continued to show a good uptrend. For capital goods orders, the data are shown in the accompanying chart. After strong gains from mid-2016 through this past fall, CAPEX orders have held essentially flat for the last two months.

Our take here is that nice gains in both exports and capital spending ignited the factory rebound in late-2016, but that exports have largely stalled in the past year, leaving rising capital spending and, lately, inventory accumulation as the main drivers of manufacturing growth of late-2017. We have wondered how long capital spending “could go it alone” (as inventory rebuilding eventually faded).

Despite our relatively downbeat outlook, we are inclined to view the two-month “stall” in capital goods orders as statistical noise. We’re ready to change that view should capital orders stay flat in early-2018, but for now, two months don’t make a trend. The most likely path for CAPEX going forward is an uptrend, especially when the effects of the recent tax bill are factored in. Apart from that, we still expect somewhat slower factory growth in the months ahead, as inventory rebuilding cools.

As for GDP, today’s news of 2.6% growth is well below Wall Street’s estimates (in the mid- to high-3-handle range) but equally above our own guess of 1.5% growth. We thought both inventories and foreign trade would provide big drags that would offset holiday spending by consumers and strong investment by businesses. A preliminary look at the data indicates that inventories were not as big a drag as we expected, but possibly more of a drag than other analysts were calling for.