In our installments of By the Numbers we have paid a lot of attention to the malaise in US manufacturing activity that has been in place since late-2012. The driving causes of this weakness have been declines in capital spending and exports. Both have shown improvement in recent months. Capital spending has clearly arrested its downtrend, although a rebound is not yet clearly in place.

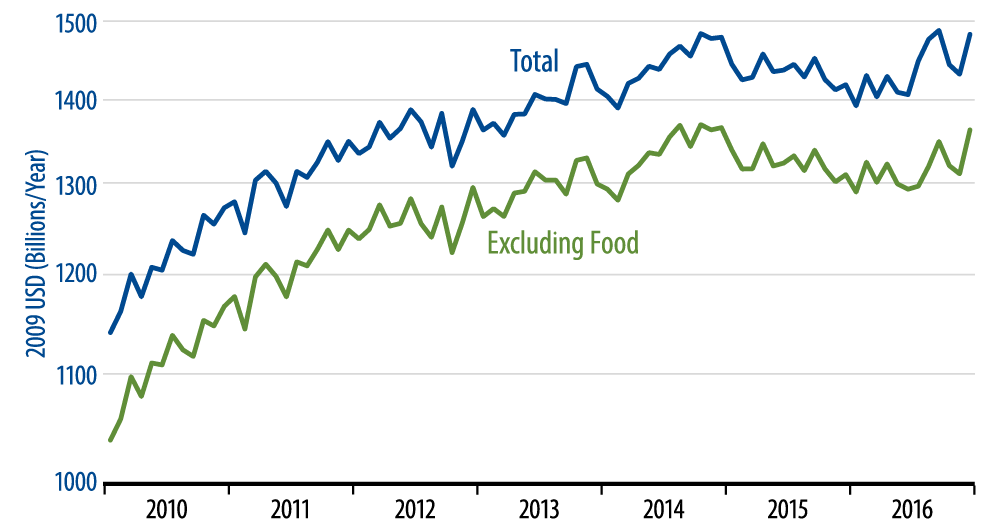

For exports, here too, the declining trend looks clearly over, and the evidence of a rebound is a bit more substantial. True, a summer surge in soybean exports distorted things, as soybean crop failures in Brazil and Argentina pushed Chinese demand to the US, and huge amounts of US soybeans were exported, largely out of stockpiles. Still, even excluding foodstuffs, we can see a mild but mostly sustained upturn in exports over the last five months (green line in accompanying chart).

No, US exports are not exploding, and the trade deficit remains a hefty 3% of GDP (with the merchandise deficit more than 14% of goods GDP). Still, we are seeing the beginnings of an improving trend in exports and a stabilizing trend in the trade balance, after constant deterioration in both for a number of years. The budding improvements in CAPEX and imports should be enough to push underlying US GDP growth back toward 2%, after a dip below 1.5% through the middle of 2016.

No, we are not reversing our forecast of continued sluggish growth. It likely won’t be quite so sluggish in the quarters to come, however, thanks to the improvements we are seeing in capital spending and exports.