2015年01月21日時点

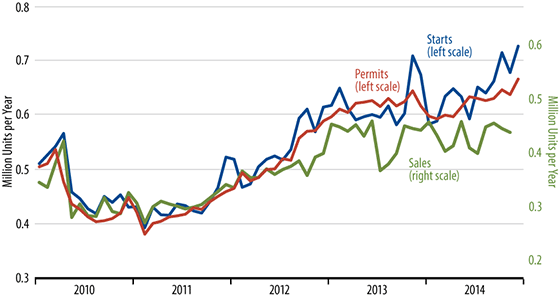

Today’s news on US homebuilding was distinctly positive. Two months ago, housing starts showed an October spike that looked flukey, in that it was not accompanied/verified by comparable increases in building permits or home sales. A similar spike in late-2013 was reversed in subsequent months, and we thought the late-2014 spike would be similarly reversed. Indeed, housing starts data a month ago showed some partial reversal of that gain.

However, today’s data for December starts showed a level of single-family starts even higher than that of October. The chart shows the single-family starts data (blue line), along with comparable data on permits and new-home sales. Notice the sustained upturn in starts in recent months.

It remains the case that recent starts levels are much higher than is consistent with recent levels of permits and sales. Nevertheless, when a data spike such as that of October starts is sustained and built upon, one has to start taking it seriously.

The backdrop is that other sectors of the economy had been showing distinct improvement in recent months. Capital spending and homebuilding were two sectors that had failed to participate in that improvement...until recently. Today’s data on starts make it look as though housing, at least, is moving in line with other sectors of the economy.

Once again, to sustain the recent gains, levels of permits and home sales are going to have to increase commensurately. Still, if nothing else, today’s data indicate that homebuilders feel confident that they will indeed be able to sell the extra homes that they are building.

Our forecast line had “faded” the increased optimism the consensus has been showing, arguing that the widely touted economic acceleration was more tentative than the consensus was claiming. The recent spate of economic data makes it hard to hold to that line.

The irony is that even with the better data and increased optimism, markets have been in a mostly risk-off mood of late. Thus, it is questionable whether the economy’s clear improvement will translate into upward pressure on Treasury bond yields.