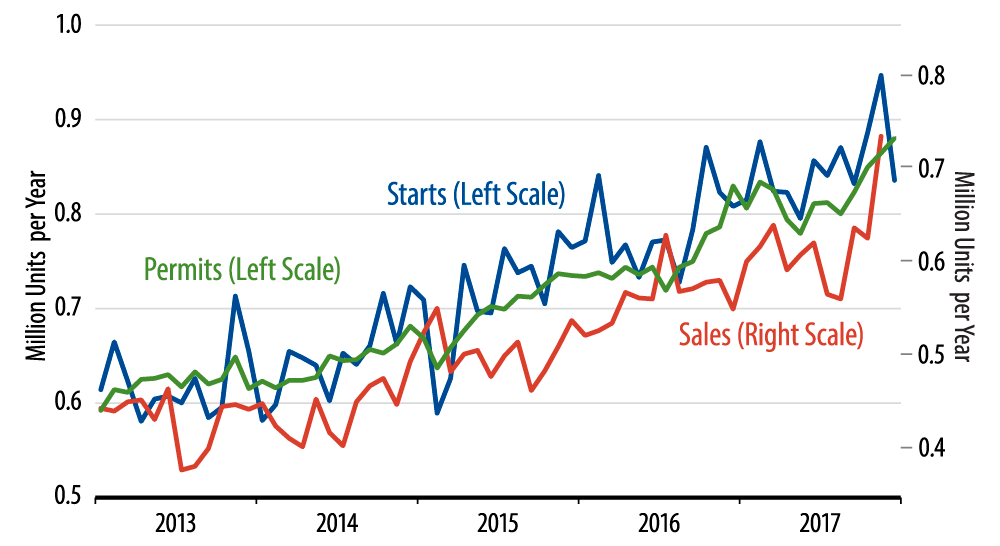

So it is with this morning’s housing starts release for December. The November release a month ago showed a sharp 5.3% increase in single-family housing starts that pulled that indicator way above previous trends. Our take was that this increase was probably not a break to a new, higher trend, but more likely a reflection of a catch-up in activity following hurricane-depressed starts in September and October.

The latter now does indeed seem to be the case, given that December single-family starts showed an 11.8% decline (from November’s revised 6.9% increase). The December decline pulls single-family starts back to levels right in line with the flat trend seen since late-2016.

Our take is that the December level, and the similar levels seen throughout 2017 until November, represent the ongoing reality. Supporting this contention is the fact that single-family starts in the South—where over 50% of US homebuilding occurs and where hurricane effects were focused—showed these same November/December swings and also descended in December back to levels right in line with pre-November, flat trends.

We have been countering the widely held contention that US economic growth has accelerated over the last few months, arguing instead that the gains seen in some indicators are one-time blips related to post-hurricane activity. So far this month, data on payroll jobs, industrial production, and now housing starts have been in line with this position, while retail sales have not. On to the next indicator!