2015年01月09日時点

Our take on the economy has been less upbeat than the consensus, and that take has been put to the test by the economic data of the last month plus. The most obvious example was the payroll employment report last month, and today’s jobs report continued the better tone.

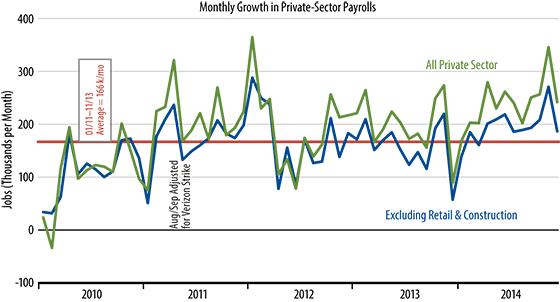

No, December did not show job growth anything like the 300,000-plus November gains reported a month ago. However, there was no “payback” this month from the especially strong gains of a month ago. Total private-sector jobs rose 240,000 in December, and October/November gains were revised higher. We focus especially closely on a jobs measure that excludes the very volatile construction and retail sectors. That measure showed a December gain of 184,000, following 269,000 in November. As the accompanying chart helps illustrate, even the December gain is somewhat above the trends of the past few years, and the November gains were way above trend.

On balance, we’ve seen average payroll job gains of 183,000 per month excluding construction and retail since November 2013 and average gains of 227,000 in total private-sector jobs over that period. Both of these averages represent accelerations from the pace of 2011–2013 on the order of an extra 0.2% to 0.3%. That acceleration is not as spectacular as the consensus buzz might suggest, but it is a notable acceleration nonetheless.

One reason our calculations don’t show a sharper acceleration is that we would still lump the weak December 2013 gains in with those of 2014. The December 2013 weakness was due to the early effects of last year’s polar vortex, so it paved the way for especially large jobs gains in spring 2014, when the weather thawed. We haven’t (yet) seen similar weather effects on the jobs data presently, so a growth calculation that focuses only on 2014 data overstates things a bit.

To repeat, on net, job growth has clearly picked up in recent months, though not as sharply as the headlines might suggest.