Cars, gasoline and building materials are excluded from control sales not only because sales of these items go to businesses as much as to households (our focus is on consumer demand), but also because of their extreme short-term volatility. Gasoline sales were up mostly on a bounce in gas prices, following two years of declines. Car sales were up on Christmas promotional deals, and, for most consumers, cars are purchased with little cash up front and lots of monthly payments down the road.

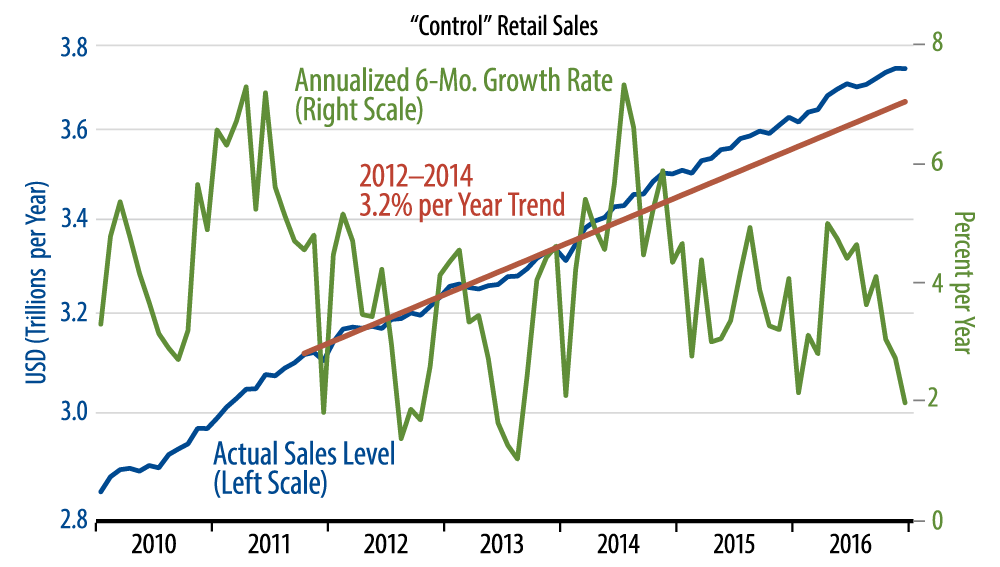

For the items in control sales, cash is generally paid either up front or next month, when the credit card bill comes in, and for these items, again, sales were flat in December. Also, as seen in the chart, for the last six months, the annualized growth rate has been a mere 2%. Now, it is true that the recent sogginess in control sales growth comes after strong growth early last year and in 2015. So, we don’t mean to assert that consumer spending is weak.

In the what-have-you-done-for-me-lately world of the financial markets, though, recent growth rates are what drive securities prices, and on this score, non-auto retail sales have been disappointing. However, this merely jibes with the slower income growth households have experienced recently from the slower growth in jobs.

In terms of store types, recent sales have been soft at electronics, book/sporting goods, furniture and department stores, better at car dealers, and steady for other sectors. In case you are wondering, toys are included in the book/sporting goods sector. For that other Christmas staple, apparel, sales continued flat, as they have for the last two years.