2015年01月14日時点

Retail sales had been the one demand-side indicator to show a clear acceleration in recent months. Yes, job growth (on the supply side) had been clearly better, but on the demand side, most indicators have shown at best steady growth, the exception being retail sales, which had accelerated noticeably in the last half of 2014.

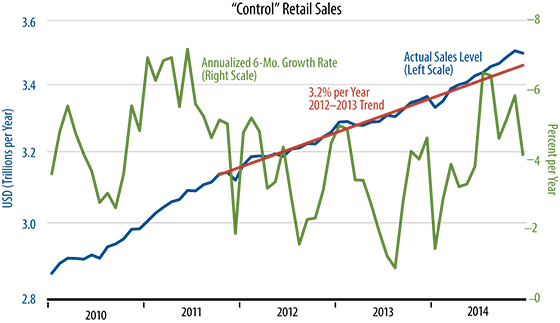

Today’s news changed the retail picture only partially. Total retail sales declined -0.9% in December, and the “control” measure that most analysts focus on declined by -0.2%. And yes, there were downward revisions to October and November data. However, even with these declines, retail sales still show a net acceleration in late-2014.

The accompanying chart tells the story. As you can see, the December decline—and October/November downward revisions—still leave the December level of sales above the trend line that prevailed from late-2011 through the first half of 2014, though surely less so than appeared to be the case a month ago.

Within sectors, sales at restaurants and at electronics, department and building materials stores all still show some net improvement. However, across these store types, only restaurants showed further growth in December.

On net, today’s data are more in line with our moderate forecast than has been the case with the general tenor of data releases since late-November. Still, we will have to see further softness in retail sales in the months to come for our forecast of 2.5% US economic growth to ring true.

Meanwhile, the net strength in the economic data over the last month failed to put any dent in the downtrend in Treasury bond yields, and bonds are rallying further on today’s news. So, while “everyone knows” that the Fed will be tightening this year and that the economy is picking up, this common knowledge has yet to be reflected in bond yields or credit spreads.